Chinese markets were closed today, so there was nothing concrete to spook or save the miners. A few iron ore plays caught a bid on the absence of bad news, with FMG up 2.3%. Generally not much movement and all we wait with bated breath for renewed signals. Plenty will be hoping a bottom is close for iron ore (aside from the shorts who’ve been piling in lately).

Roy Morgan released its Australian business confidence survey, which recorded a slight dip from last month. The survey has declined markedly from its post-election high last year, and is now below the average level of the past 4 years. Most worrying, overall sentiment is being underpinned by ebullience in the finance and real estate sectors, reflecting the strong housing market, while sectors such as retail, manufacturing and construction are all in the doldrums. Not a reassuring combination for anyone concerned with Australia’s post-mining boom structural adjustment. Tomorrow we’ll get the more closely-watched NAB business confidence survey, which has been showing decidedly more upbeat corporate sentiment of late (down only slightly from the post-election high).

Also released today was the ANZ job ads survey, which continues to show a modest improvement in labour market conditions, registering a 1.5% gain over the month. Chief Economist Warren Hogan noted that this appears at odds with the last employment data from the ABS, which recorded a sharp increase in the unemployment rate to 6.4% from 6% the month prior. The next employment report is out on Thursday and is expected to show an increase of 15k jobs and a drop in the unemployment rate to 6.3%. It’ll be very interesting to see how this release goes, given the signs of a gradual thawing in economic conditions, which must nevertheless be set against the looming menace of falling mining investment (to say nothing of the terms of trade beat-down).

The big story today however was Chinese trade data. The trade surplus came in at a record $49.8bn, and well above expectations for a $40bn surplus. Exports were up 9.4% for the year, following a 14.5% rise in July. Adding to the surplus was the decline in imports, which fell 2.4% after a 1.6% drop in July. While these figures are positive for China, a mrs pressing concern for this blog is the welfare of Australia; and despite appearances, what’s good for China is by no means good for Australia.

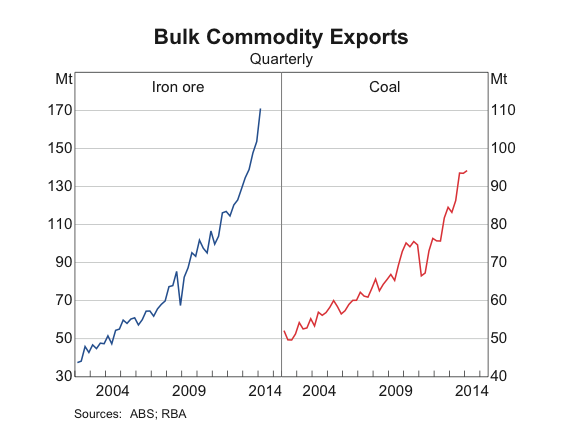

Buried within these data are some worrying portents for Australia. Coal imports slumped to 18.86m tonnes in August, the second month of decline and the lowest since September 2012. The promise of coal has long passed for Australia, but it remains noteworthy all the same that domestic prices in China are sitting at 6-year lows. More important than the drop in coal imports was that of iron ore, which fell 9% from the previous month.

The official party line throughout the ore rout this year has been that it’s a supply-side issue; soaring output is weighing on prices. The corollary being that while there may be lower prices these days, Australia has ramped up exports to compensate. This has it’s own set of problems for juniors, of course, whose business models don’t compute at lower prices, but for the most part it’s been an accurate appraisal of the market. However, as the esteemed David Llewellyn-Smith noted last week, “there are good reasons to be concerned that what started as a supply side issue for iron ore is very quickly swinging to a demand side problem for steel.”

Unfortunately, today’s trade data, in conjunction with recent steel output data showing a sharp drop off this month, suggest we are indeed beginning to see cracks in Chinese iron ore demand. No doubt there is a seasonal element to the fall in steel output and thus ore demand, but it has been an unusually large fall and, moreover, this simply reinforces the fact that without more fixed asset investment-driven stimulus, we just aren’t going to see a lift in steel demand, steel output, and iron ore demand that is anywhere near big enough to mop up the supply deluge.

Expect more iron ore price pain and a comparatively listless rebound when it comes.

{kind=link}