Drowning in Jobs

Yesterday I said the market would be looking for a strong result from today’s employment report, along with reassurances that last month’s leap in the unemployment rate was a ‘statistical aberration’. Evidently the ABS has a sense of humour, because calling today’s report a statistical aberration significantly undersells it.

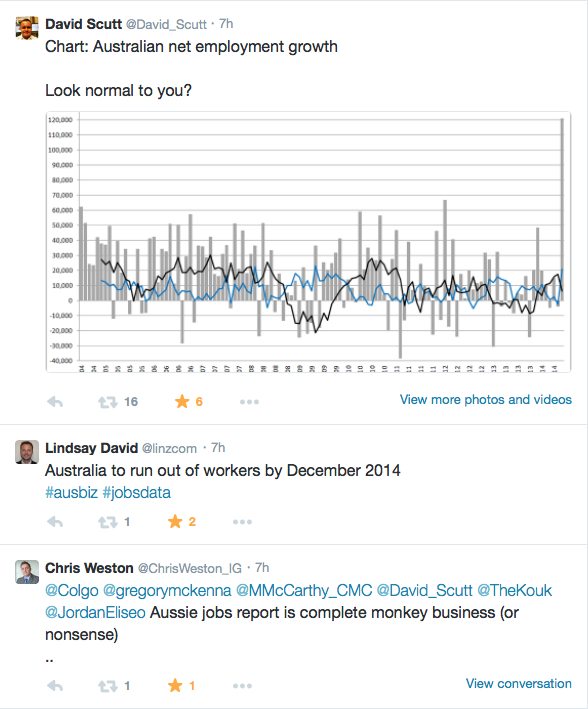

Supposedly 121k new jobs were created in August, in seasonally-adjsuted terms, with the labour force participation rate jumping and the unemployment rate diving back to 6.1%, from 6.4% last month.

Unsurprisingly, the result met with swift derision.

As far as interpreting this data goes, it’s best to ignore the seasonally adjusted figure, which has long been renowned for it’s volatility, and instead focus on the trend. On this, the news was still reasonably good, with 18k jobs created, however the unemployment rate ticked up to 6.2%. The headwinds for jobs do still remain owing to Australia’s poor competitiveness profile, however fast-moving developments in the currency markets suggest some relief may be in the offing.

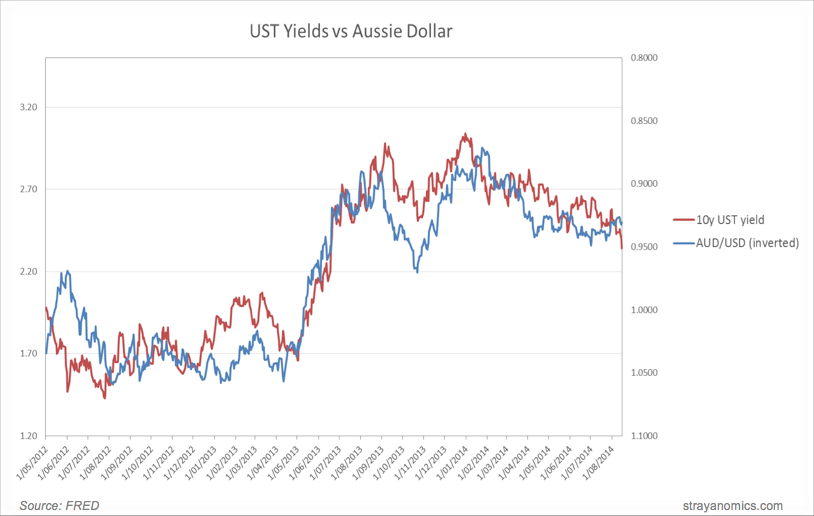

The price action on the Aussie battler was particularly informative. The algos leapt at the enormous beat, and pushed the AUDUSD back above the key .9200 support level which had been taken out in the previous session. This didn’t last long though, with heavy selling pressure arriving each time it retested .9200 in the afternoon. Once it was clear this level would not be re-established, the once-indomitable Aussie battler quickly gave up the fight.

This suggests a fairly aggressive unwind of the popular leveraged carry trade, with longs looking to get out before the all-important Fed meeting next week. Now that this range has been decisively broken, it will take a very dovish Fed to prevent a move down to the .9000 and below.

The bias is clearly lower; a break of critical support, followed by a retest and rejection after an extremely bullish (if noisy) data release, very bearish price action.

I’ve had a bearish long-term view on this old boy for about 3 years. The voracious global yield hunt has supported it this year, helping it to gleefully brush aside the unfolding terms of trade bust (the booming domestic housing sector did the rest). There’s no assurances that the Fed won’t once again massage down expectations of tighter monetary settings, but the stage is definitely set for a substantially lower AUDUSD.

It took the market’s wild taper tantrum last year to really send the AUDUSD into a tailspin.

We probably aren’t going to see such a violent sell off in bonds this year, so the pace of the sell off isn’t likely to be a ferocious. But a stampeding exit from the carry trade combined with sizeable re-positioning of shorts provides plenty of scope of a decent down move in the near future.

Stay tuned for the Fed.

Iron ore

The market is now quite clearly searching for a bottom. Futures contracts have stabilised in China in the past two sessions, which has typically signalled a turn. It looks as though we’ll only see spot prices in the 70s only briefly on this move, if at all. Alas, steel remains weak. Consequently, Chinese steel mills are running on razor thin inventories, reluctant to tie up more capital than they absolutely need to. This provides the conditions for a healthy rebound in spot iron ore prices if and when the steel price recovers and mills replenish their inventories of iron ore.

This is what the miners, and the bullish sections of the sell-side, are pinning their hopes on. There’s wide scope for disappointment here. Steel capacity in China is enormous, any turnaround in prices will be met with a rapid expansion in supply, and so prices are likely to remain in structural decline unless demand stages a heroic recovery. This I do not believe is likely, as I’ve outlined previously. Therefore I expect the inevitable rebound in spot iron ore prices to be quite muted, certainly by the standards of late 2012. If property doesn’t improve soon, then there is the risk of little seasonal rebound in iron ore prices at all.

I’ll stick my neck out and say I’m looking for a recovery just above $90 on the reversal of this down move, peaking in December, before the next leg down form January onwards, which will drive out all Australian juniors who produce at a break-even above FMG. Whether FMG can wrench its costs down fast enough to survive the reckoning is going to be one of the most enthralling corporate melodramas of our day.

It’s encouraging to see signs that iron ore futures are stabilizing.

LikeLike