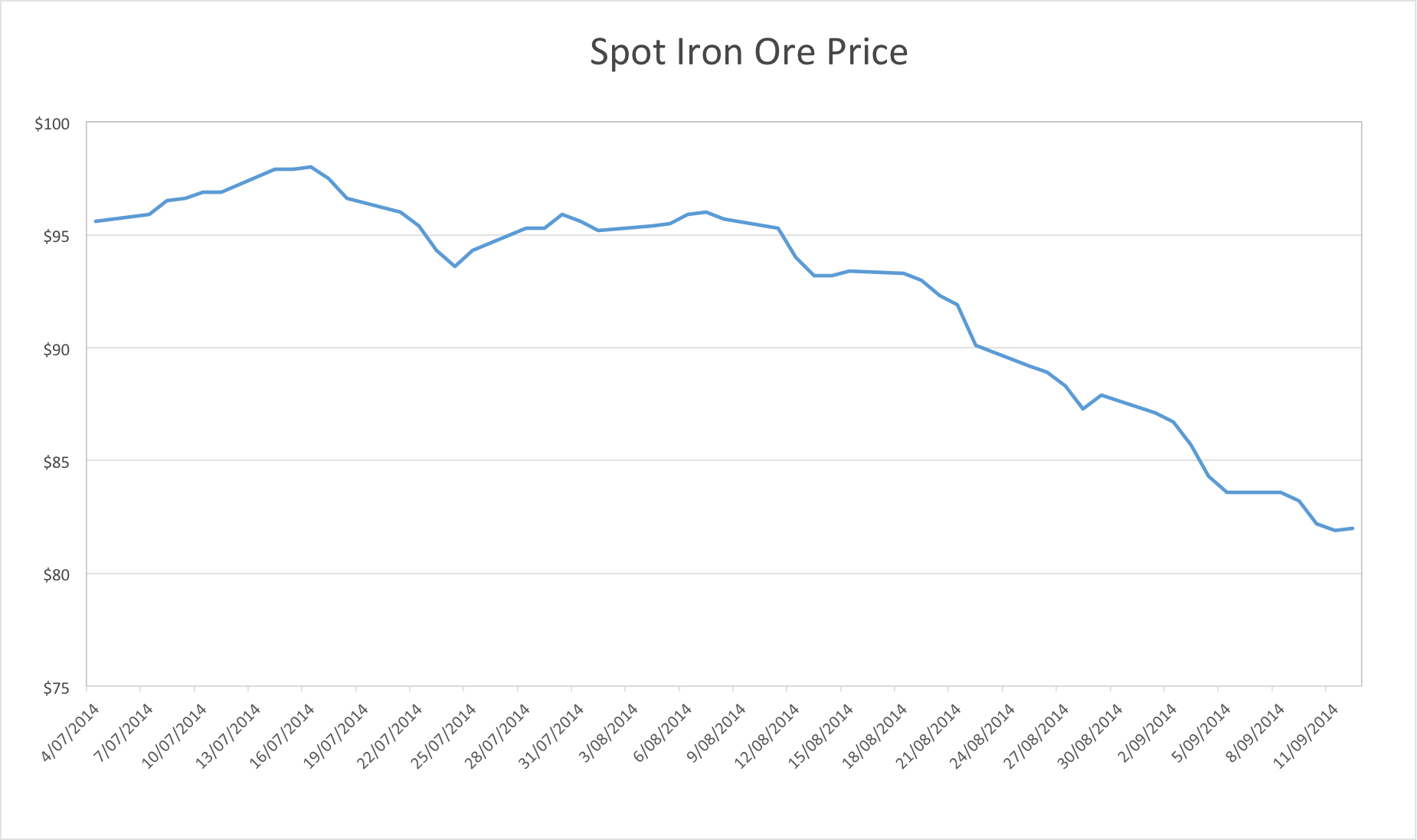

This was supposed to be a fairly upbeat post courtesy of iron ore’s more positive price action this past week; spot fell 1.9%, after dropping close to 5% the week prior. Although it was the fifth consecutive week of declines, there was clear indications that the market was bottoming for the time being.

Steel futures managed to eke out a small gain on friday, as did spot iron ore. Dalian iron ore futures dropped like a stone on wednesday before staging a heroic recovery, and although spot dropped that day it was stable into the week’s end, suggesting the worst may have been behind it, at least in the short-term.

Chinese data dump muddies the pond

Alas, the good news ended there with a fairly miserable set of figures from China’s stats bureau yesterday.

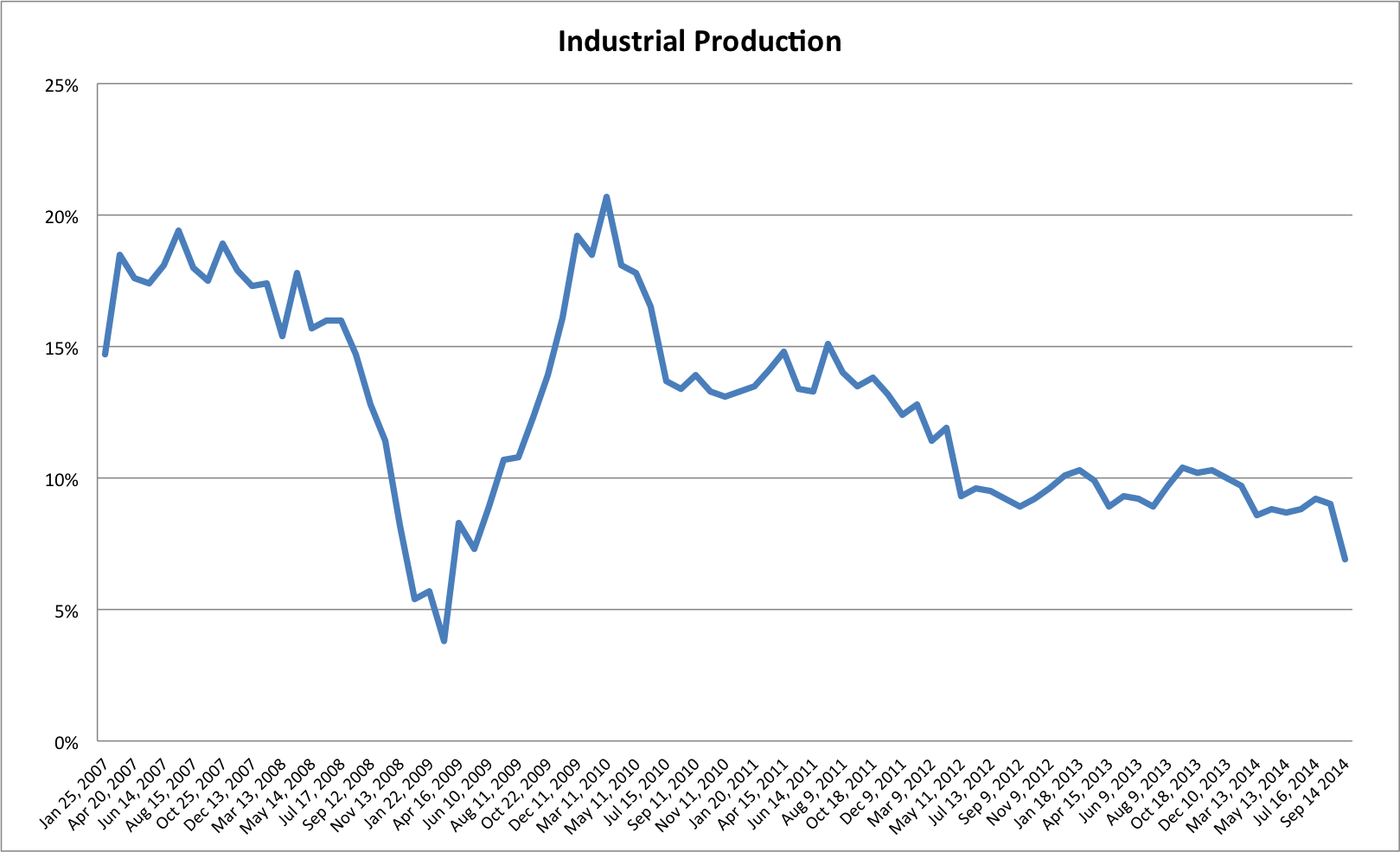

Growth in industrial production plummeted to 6.9% in August, down from 9% in July, on expectations of 8.8%.

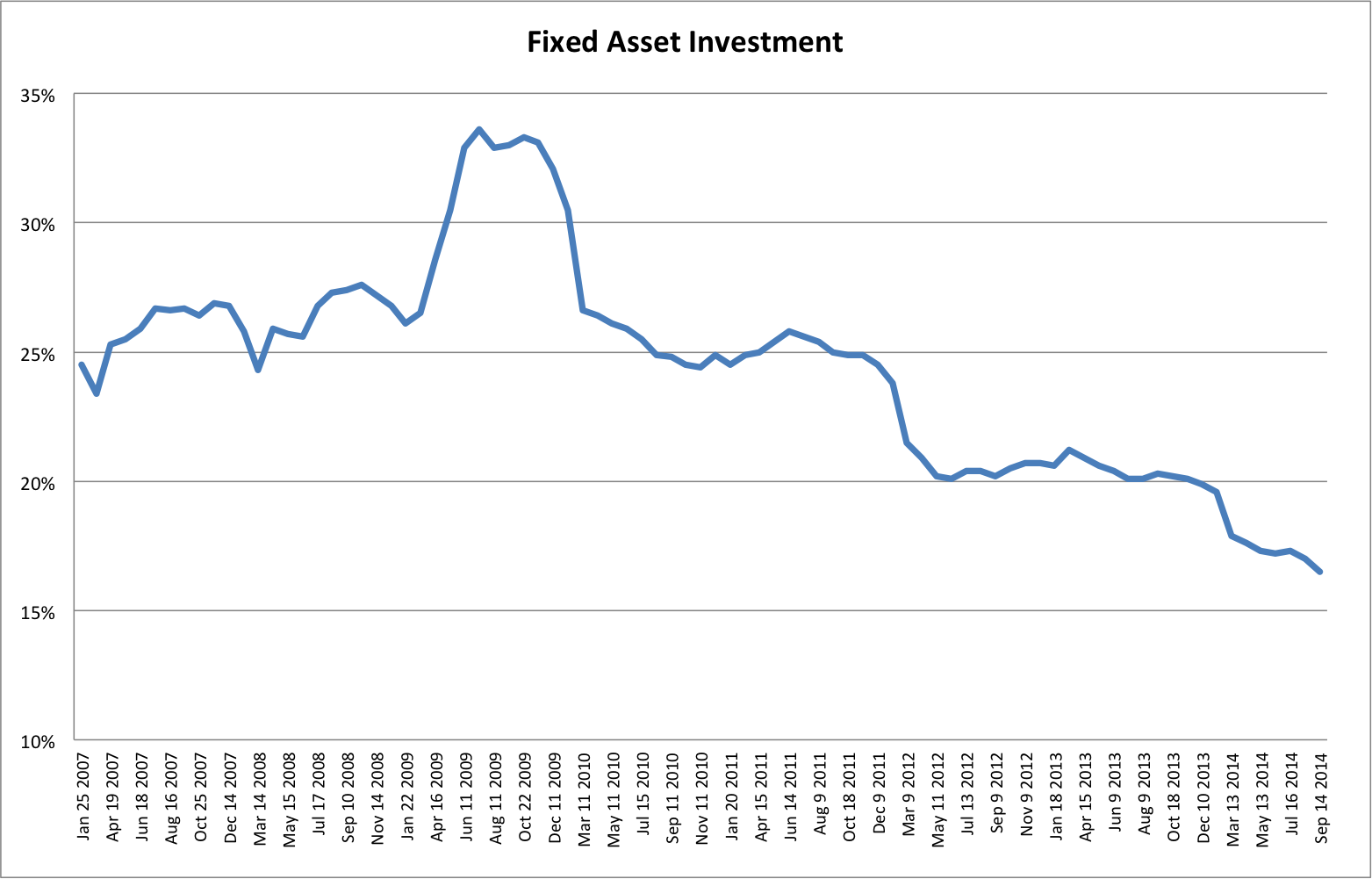

Fixed asset investment (the long-time driver of Chinese growth), came in at 16.5%, form 17% last month, well below expectations for 16.9%.

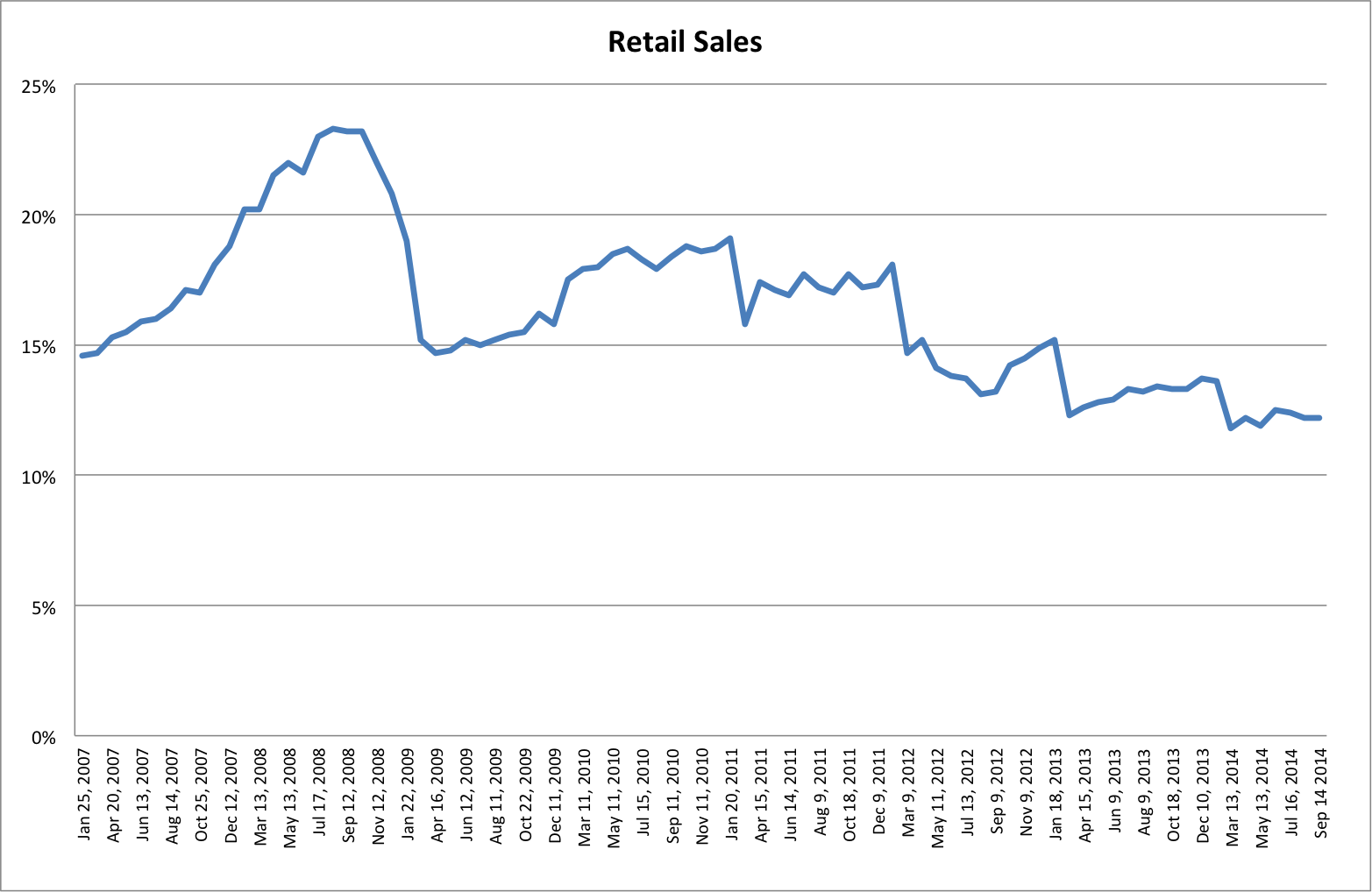

Retail slipped as well, to 11.9%, down from 12.2% on expectations of 12.1%. They’re holding up better than FAI, which is a plus for Chinese rebalancing.

In the most basic sense, for China to successfully rebalance, retail sales need to grow faster than FAI for an extended period, such that the investment share of GDP declines from its extraordinarily high levels it reached in the aftermath of the financial crisis.

China, as with all countries in the early phases of development, has long been characterised by elevated levels of investment. However, in response to the Asian financial crisis in 1997-1998, China pushed its investment share up to defend its growth rates. This effectively meant China was growing more and more dependent on external final consumption demand. This was fine as long as China could run very large current account surpluses with the rest of the world. However, when the global financial crisis hit, this foreign demand dried up, and China doubled down on internal investment demand (in infrastructure and property, primarily) to support growth.

In so doing it saw its current account surplus shrink as it sucked in imports of raw materials and suffered the loss of demand for its manufactures. Investment’s share climbed to levels virtually unseen in large economies. The issue was, without large current account surpluses, China had to flood its own economy with credit to support extremely high levels of investment.

Rebalancing therefore means investment growing more slowly than consumption, as well as credit growing more slowly than nominal GDP. Credit growth has slowed, but it will need to remain at roughly the pace it is at present if China is to meaningfully rebalance its economy. The trouble is the economy is blatantly running out of puff each time credit and/or investment slows.

The central conundrum of the rebalancing process is that consumption falls when investment falls (since income is reduced) and nominal GDP growth slows when credit growth slows. How far each of these must slow before the the economy reaches a sustainable state is not known. But it is ever-more apparent that it’s not going to be as smooth a transition as the China bulls expect (‘believers’ is a preferable term to bulls, I think, in keeping with Michael Pettis’ terminology).

Market reaction

How the markets react to this in the coming week is going to be very interesting. The calls for stimulus will be deafening now, and the government is likely to respond with supportive measures of some kind. I still find it highly unlikely that an about-face is coming regarding ‘big bang’ investment stimulus, and the markets are going to be very disappointed if that turns out to be the case.

An exciting week ahead!