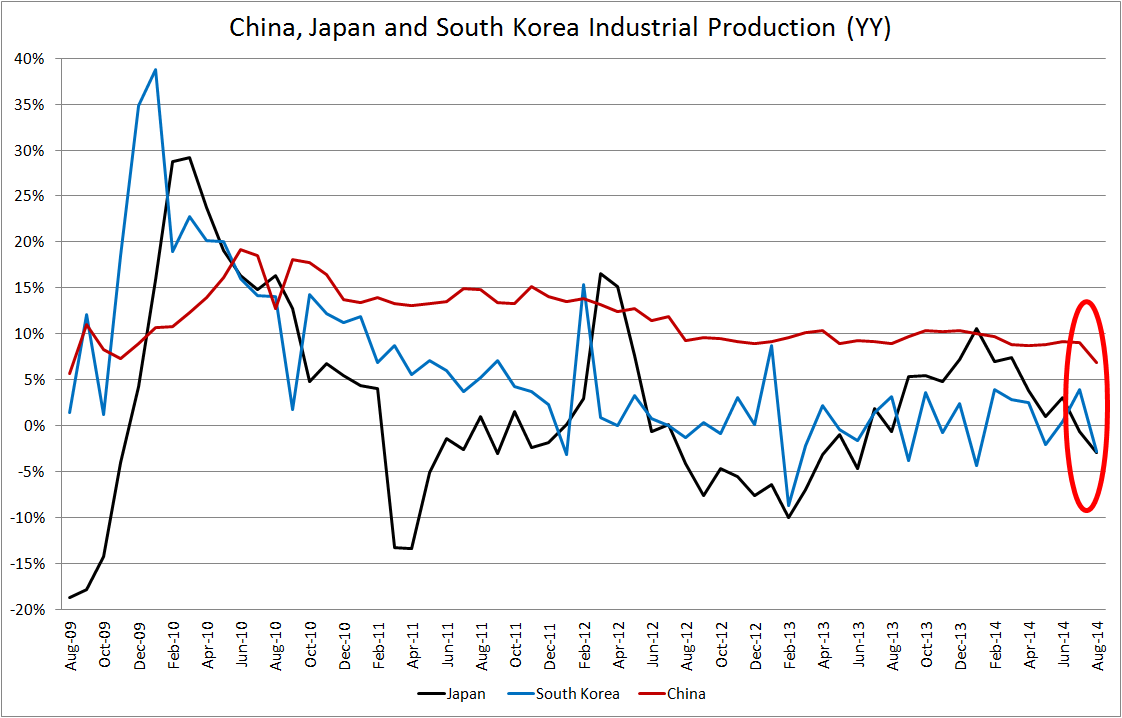

Softness in Asia

August Industrial production (IP) figures were released today for South Korea and Japan, and both were weak; -2.9% for Japan and -2.8% for Korea, both year-on-year. Close to a third of Korean exports and one fifth of Japanese exports go to China, so the recent slowdown in Chinese industrial production and surprise fall in profits are likely to be contributing to regional weakness. This chart from David Scutt paints the picture:

Apart from the always-suspicious absence of volatility in Chinese figures (the latest print did buck the trend there, I suppose), the trend in Japanese IP is clearly of concern. The rebound in IP in 2013 occurred largely as a result of a massive depreciation in the yen, seen in a 33% rise in the USDJPY between late 2012 through to the end of 2013.

Two things happened this year; until August the yen was broadly flat, and in April the government raised the sales tax. Since the sales tax hike, IP has fallen in 3 of the next 5 months (month-on-month).

The USDJPY has rallied hard in the past few weeks. It remains to be seen if this can invigorate Japan’s languid industrial sectors. It will undoubtedly help at the margin, but a larger unknown is the outlook for Chinese production, which is of course mostly dependent on the ‘will-they-or-won’t-they’ stimulus outlook.

On a related note, there was a good article in last week’s Economist on Japanese and Korean firms’ tendencies to hoard cash to the detriment of their economies. At the very least, if corporates are concerned with their competitiveness and reluctant to raise wages, dividends should be increased. It would provide a welcome boost both domestically and internationally.

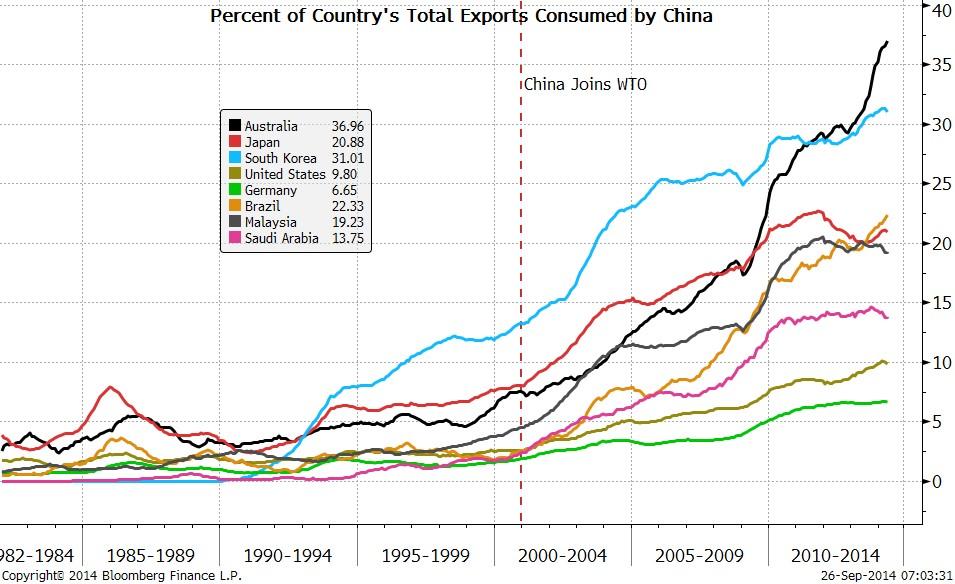

And lastly, while we’re on the topic of a heavy reliance on China, we might as well remind ourselves of some of the other noteworthy countries in that category.

Chart from Michael McDonough of Bloomberg

HSBC PMI not as buoyant as first thought

The final reading of the HSBC PMI for China was released today, and contrary to the earlier ‘flash’ estimate which had it rising to 50.5 from 50.2 the month prior, it was actually unchanged. While it is welcome to see this figure in positive territory (having spent much of the past two years in negative), the tepid expansion is only being realized via strong export orders.

As I said at the time of the flash release, the strength of exports is likely to be in partly underpinned by Chinese steel mills dumping their unsold stock into global markets, where they can achieve a much higher price than in China. This is of course vulnerable to protectionist responses from governments should their local steel sectors grow tired of ‘making room’ for heavily discounted Chinese steel products.

Moreover, from Australia’s point of view, it is hardly reassuring that the Chinese steel sector is facing such lacklustre demand locally that it is being forced to turn offshore with increasing urgency.

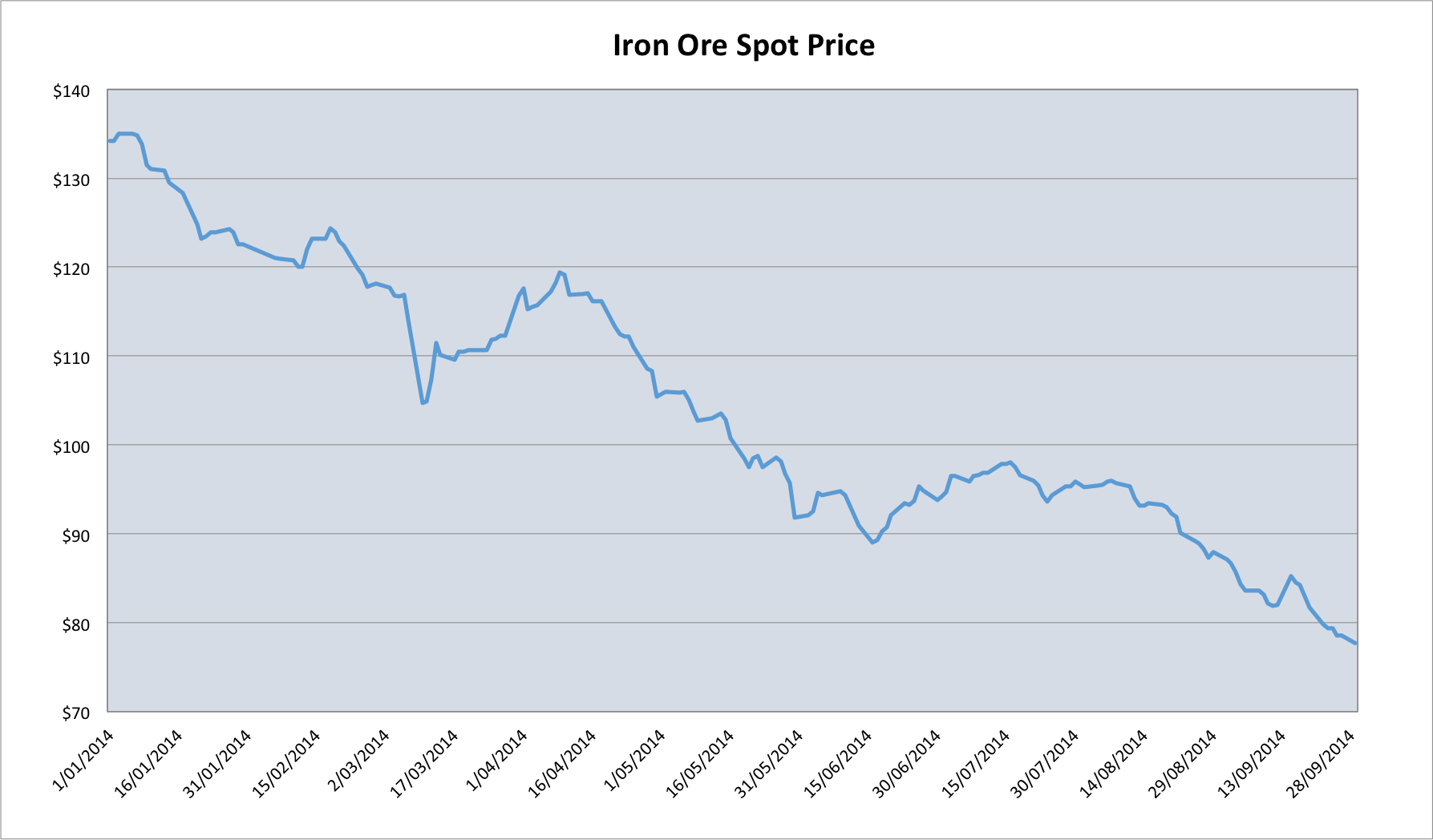

Steel-ore complex

Chinese steel futures retraced their gains late on Friday, and iron ore finished the week flat after looking like finding some buyers during the day. Protests in Hong Kong weighed heavily on prices at the open yesterday, though they gained somewhat throughout the session. Spot iron ore finished last night at $77.70, off 1.15%. It is now down 42% for the year in USD-terms, and 40.80% in AUD-terms. The recent decline in Australian dollar (or rise in the USD, really) has therefore come at a welcome time, though there is much work to be done on that front.

After rallying earlier in today’s session, the most-traded rebar contract closed down .4% in Shanghai today. Dalian iron ore gained .7%. Since markets will close for China’s National Day Holiday tomorrow, spot will need to recover yesterday’s loss to avoid an 8th consecutive week of declines. More from Reuters.

In local news, ex-RIO chief Anthony Albanese has joined ex-BHP executive Alberto Calderon in expressing his scepticism regarding the oft-cited iron ore rebound supposedly arriving later this year (if it comes, late October would be my guess). As a reminder, in Q4 2012 spot pieces soared after collapsing on seasonal weakness, and a similar pattern is seen by some as a possibility this year.

Of course, I’m in agreement with Calderon and Albanese that we won’t see a pronounced rebound this year (bearing in mind that no one, to my knowledge, is expecting the rebound to produce prices comparable to 2012).

To reiterate, my reasons for this are:

- India knocked some 100m tonnes of annual supply out of the seaborne market fairly rapidly in 2012 with its ban on mining in Goa, which followed similar restrictions in Karnataka in 2011 (total traded iron ore was about 1100m tonnes in 2012). If memory serves, Macquarie reckoned these moves added about $20 to spot prices throughout 2013.

- Chinese stimulus via fixed asset investment flowed freely in 2012, and, critically, the property sector commenced a strong upswing around the time iron ore bottomed. Property is moving in the opposite direction now, and like much else in the Chinese economy, oversupply is becoming an issue. It remains to be seen whether the government is prepared to allow this process to run, or whether they cave and unleash another ‘big bang’ stimulus, as many analysts and commentators are now clamouring for. My base case is that the government institutes mild stimulus measures to support overall demand, without igniting another explosion of shadow banking excesses or wasteful fixed asset investment. But it’s roulette really, all you can do is monitor the situation in Beijing closely.

- Due to a renewed upswing in Chinese demand, the loss of Indian supply tightened a market in which suppliers already held considerable pricing power. As everyone is surely aware, that is no longer the case now, with Morgan Stanley putting this year’s surplus at around 50m tonnes, growing to 150m next year. It has decisively shifted to a buyers’ market.

- The displacement of high cost supply, which the majors adduce to justify their enormous supply expansions, will help stabilise prices in time. But so far this has occurred much more slowly than anticipated, and I expect this continue and high cost supply to exit only incrementally, rather than in a rapid manner that shrinks available supply and compels Chinese steel mills to suddenly scramble for stockpiles.

Thus, short of a ‘big bang’ stimulus from the Chinese government, the recovery in spot iron ore later this year is likely to be much more muted than in previous years. I still would not be surprised to see it rebound to around the high-$80s, but there is a good chance that the impetus for Chinese steel mills to restock as they typically did in the past just isn’t there now that the market is firmly in structural surplus.

Update

Spot fell to $77.50 today, 8th week of declines, down 12% for September. Again, I’d be surprised so see another monthly decline in October as it usually ushers in restocking activity; it’ll be interesting to see if tradition is upheld this year!

{kind=link}