RBA day

Well, what a day to return to the world of econ after a long weekend of agreeable company and responsible drinking.

The Treasurer has acknowledged that the terms of trade bust is likely to weigh heavily on the budget in the years ahead, which seems to have spooked bank stocks (Australian banks funding costs are dependent on the health of the public balance sheet). Although I am in agreement on the outlook for commodity prices, it’s worth bearing in mind that the budget in May expected the Australian dollar to remain at .9300 against the USD. The large falls in the AUDUSD during the past couple of months will therefore help to cushion the impact of the prices for key exports (by supporting company tax revenues).

The RBA will chime in shortly with its view on the state of the economy. There’s effectively zero chance of the RBA changing the cash rate today, meaning my dovish forecast will survive another month.

Perhaps the most impactful development in the last couple of weeks has been the RBA’s Damascene conversion to Church of Macroprudential (see here also). Bloomberg picked up the story on the weekend, with RBA Makes Hawks Cry With Turn From Rate Tools: Australia Credit.

The article quotes forecasters who’ve pushed out their expectations for rate hikes due to the change in policy from the RBA.

TD Securities and AMP Capital Investors Ltd. joined traders in drawing back from forecasts for early rate increases in response to policy makers’ hardening rhetoric on curbing mortgage lending to housing investors. RBA Governor Glenn Stevens is forecast to keep the benchmark unchanged at a record low tomorrow.

It is indeed true that the RBA’s adoption of macpru tools, if they prove successful in cooling the investor housing feeding frenzy, will reduce the need for higher rates. To recap my well-worn view on Strayan rates: the unfolding terms of trade shock and the decline in mining investment are currently jostling with a robust housing sector, concentrated especially in Sydney and Melbourne, for primary influence on the short-term direction of interest rates. So if the RBA can find ways to take the froth out of the housing market without raising rates, this favours interest rate doves.

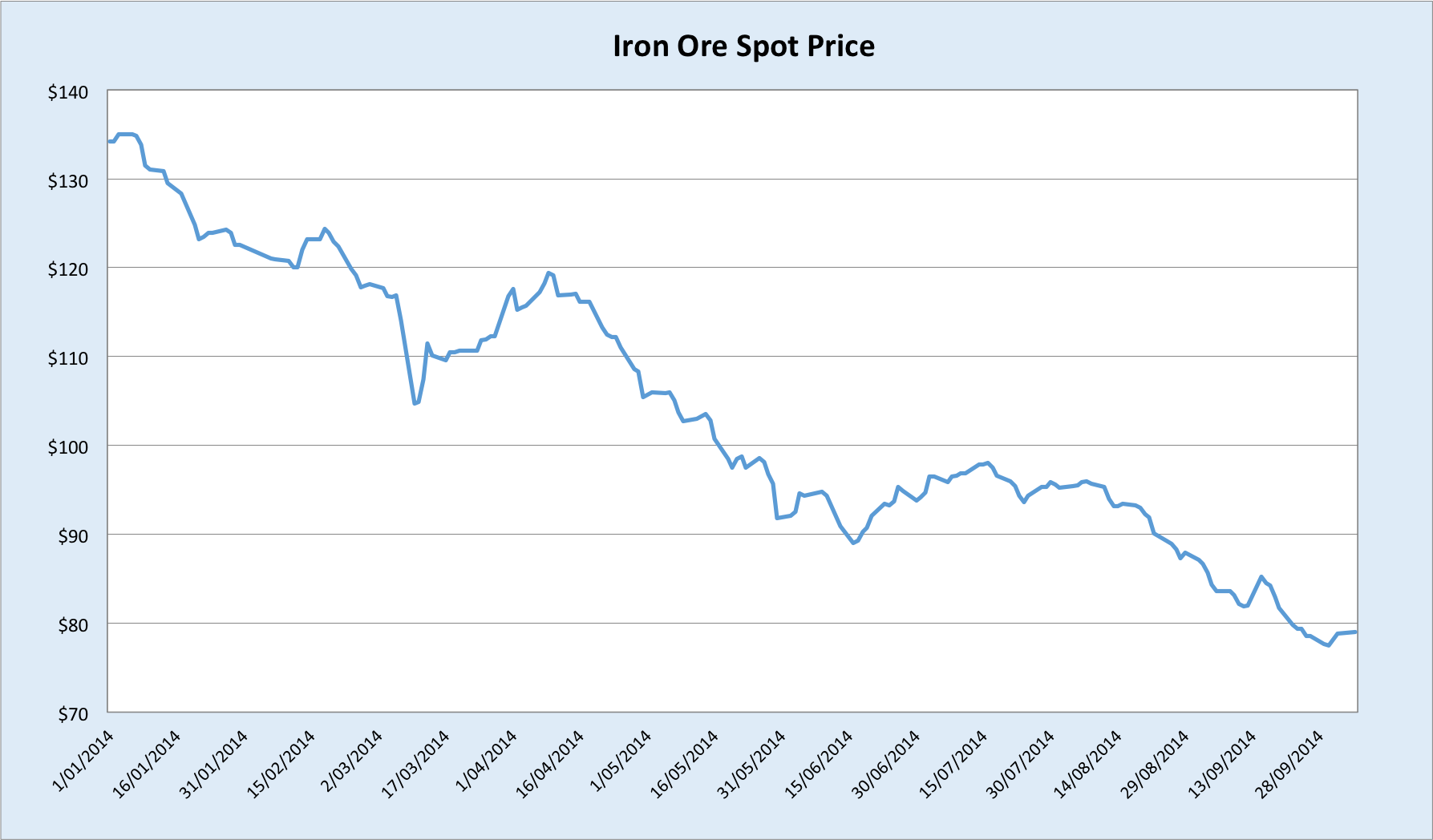

We know what the situation looks like for iron ore and mining investment.

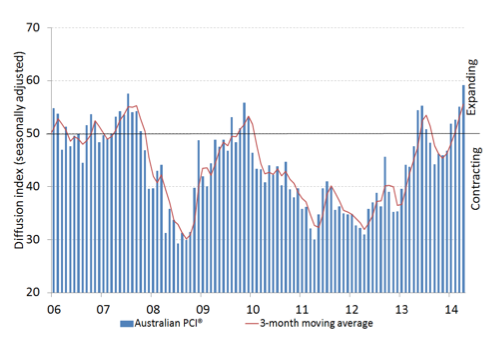

Turning to the bullish influences, activity centred on the property sector is clearly very strong at the moment, as we can see this in the latest reading on construction activity from the Australian Industry Group.

Unlike the manufacturing and services sectors, construction is charging (above 50 indicates expansion):

It is good to see a supply-side response in the property sector, since structural supply constraints have hampered the market for years. But it must be remembered that this cannot sustain the economy indefinitely. Once a house or apartment is built the positive impact on the economy has mostly passed. Of course, it provides a place to live, but living in an apartment doesn’t support jobs; building it does. Therefore other sectors, especially the non-mining tradable sectors, need to be revitalised to fill the void left by the declining terms of trade and support jobs in a sustainable manner. To achieve this means substantially lowering the real exchange rate. Raising interest rates now would severely diminish the prospects for a continuation in the currency’s fall, and make the goal of a lower real exchange rate all the more challenging.

It would be nice to suppose some excitement will be injected in monetary policy after soporific missives from the RBA, but I suspect they will be content to stand pat for the rest of the year for some time yet.