Seems unlikely. All 26 economists surveyed by Bloomberg are calling a cut at the May meeting, taking the cash rate to 2%. Likewise, rates futures are pricing a 79% probability of cut.

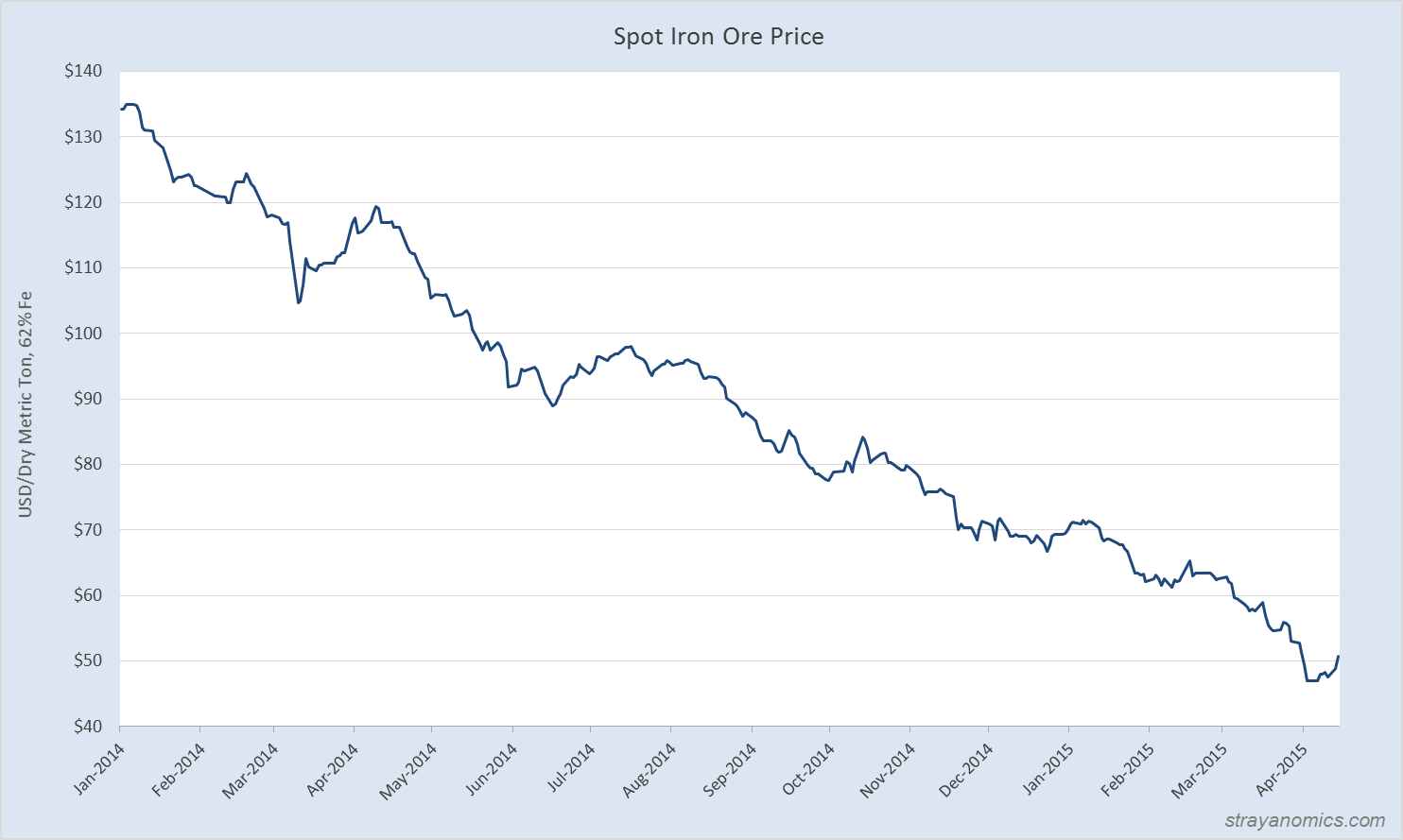

Many found the RBA’s decision not to cut last month quite bemusing, what with the 25% collapse in iron ore prices since the March meeting, the rapidly approaching capex cliff, and the need for an ongoing real devaluation if we’re to see a meaningful revival in non-mining tradables. The reason for holding, however, was clear enough: the RBA is spooked by the investor mortgage Frankenstein it has unleashed, and would rather not cut unless it absolutely has to.

My hard-fought call last year that rates would fall before they rose was validated in February, but it bears remembering how heavily I stressed the bipolar nature of Australia’s economy. I believed rates would fall, but only because the structural weakness emanating from the slide in the terms of trade and the capex wind-down was going to overwhelm the cyclical boom in the property space.

Following the February cut, the cyclical factors have truly roared, so much so that I am now wondering if the balance is tipping in favour of further reticence on the part of the RBA.

Firstly, iron ore has bottomed for now and has put on a good 8% from the (admittedly very low) lows, with Chinese futures having been locked limit up (+4%) for the past two sessions.

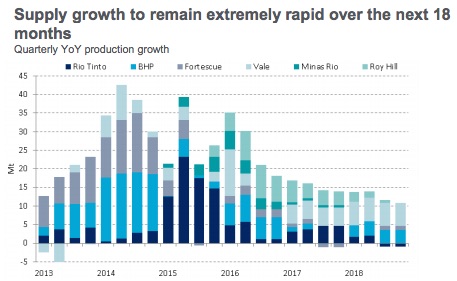

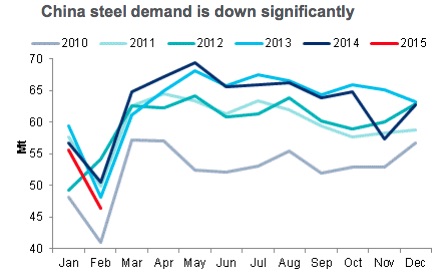

I don’t anticipate this being much more than a moderate bear market rally, for the simple reason that the market is structurally buggered. A couple of charts from Citi this week illustrate the point.

New supply is still pouring in:

And I’ve discussed many times previously, we’re almost certainly past the peak in Chinese steel demand:

But if iron ore can hold it’s gains and perhaps add another 5-10%, the RBA may well side with cyclical argument for holding monetary settings steady.

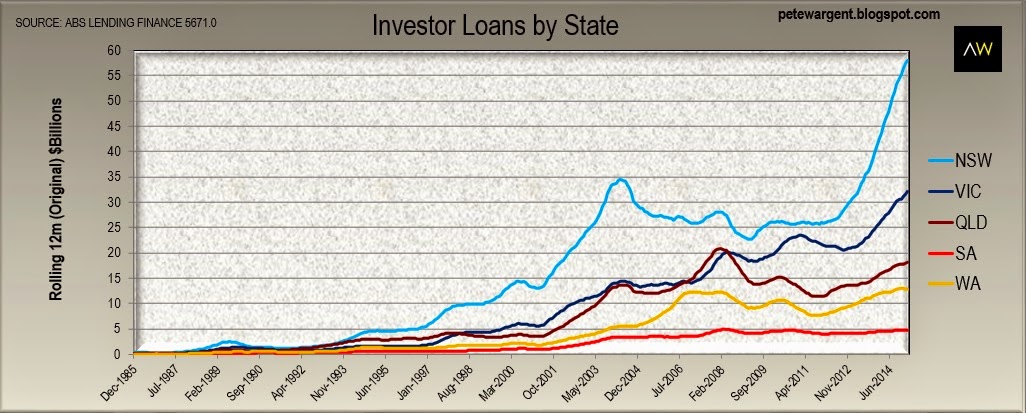

Property markets in Sydney and Melbourne have piled it on since February, and I get the feeling the RBA is especially concerned by just how sensitive activity in this space has proven to the last cut.

Investor mortgage growth in the boom states, especially NSW, remains extraordinarily strong, as shown on this chart from Pete Wargent:

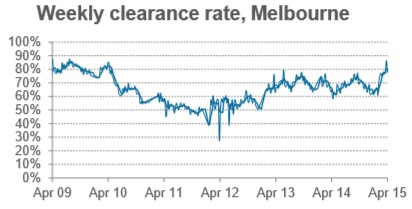

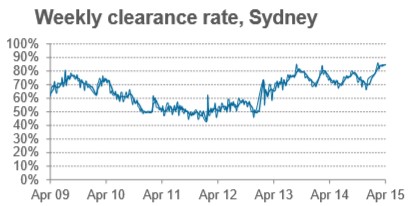

And perhaps the most important real-time indicator, auction clearances, are also pointing to exceptionally tight markets.

Viewed in isolation, this is not an environment a sane central banker could comfortably ease into. But of course it cannot be isolated from the external shock bearing down on the economy, and therein lies the RBA’s mighty quandary.

If Oz data remains benign over the next few weeks, and the iron ore price doesn’t crash through the lows before the next meeting, I suspect there’s a better chance of a hold than rates markets are pricing, and much better than economists are forecasting.

To the caveats: Firstly, the China national accounts data dump tomorrow morning could be a shocker. If it’s really nasty then the market will have to decide whether to buy on the promise of stimulus, or sell on reality. If nasty data snuffs out the metals rally, the chance of a cut obviously firms. Secondly, I expect the Fed to be dovish again at its meeting at the end of the month, and if this adds to unwanted AUD strength, the RBA’s hand may well be forced by FX markets.