Reigning in a credit bubble before it bursts is a mightily taxing task. China’s authorities have been holding firm admirably in the face of China’s cooling economy, but the chilliest property market in a long while has at last provoked a response: tonight the People’s Bank of China cut benchmark interest rates for the first time since July 2012.

Bloomberg has details:

The one-year deposit rate was lowered by 0.25 percentage point to 2.75 percent, while the one-year lending rate was reduced by 0.4 percentage points to 5.6 percent, effective tomorrow, the People’s Bank of China said on its websitetoday.

The reduction puts China on the side of the European Central Bank and Bank of Japan in deploying fresh stimulus and contrasts with the Federal Reserve, which has stopped its quantitative easing program. Until today, the PBOC had focused on selective monetary easing and liquidity injections as China heads for its slowest full-year growth since 1990.

…

Aggregate financing in October was 662.7 billion yuan, the central bank said Nov. 14 in Beijing, down from 1.05 trillion yuan in September and lower than the 887.5 billion yuan median estimate in a Bloomberg survey of analysts. New local-currency loans were 548.3 billion yuan, and M2 money supply grew 12.6 percent from a year earlier.

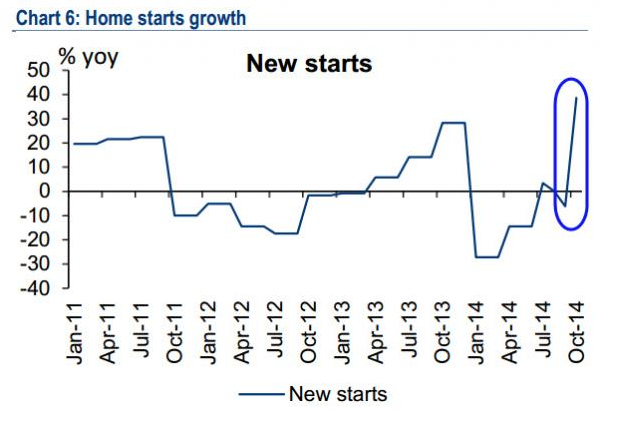

As that article notes, credit growth in October was weak despite the widely-publicised shift to looser mortgage conditions in September. This change in policy stance provoked an avalanche of new property starts, which will in turn keep the pressure on prices.

This interest rate cut does look entirely appropriate in the context of China’s economy today, and to be honest there was little choice for the PBoC given the extraordinary depreciation in the yen and signs that the ECB could be joining the party before too long. (See this post for more on that.) The economy has continued to weaken in the past few months, and although it’s too early to judge the effects of recent changes to mortgage lending rules, it does seem that more needs to be done to arrest the decline in property prices, especially seeing as the market is now almost certainly structurally oversupplied (a point that was less clear in 2012, when property last turned down).

As I’ve emphasised many times on this blog, one of the trickiest things about forecasting Australia’s short-term outlook is the ever-present Chinese policy enigma. Many commentators are eager to point out that China’s slowdown this year, with its knock-on effects to Australia’s key export commodities, has been purposely engineered by its masterly policymakers. Thus, when things look like slowing down too much, all that needs to be done is a slight easing off on the brakes and a light tap to the accelerator, and all will be well.

The obvious problem with this appraisal is that China’s debt levels have exploded since 2008 under the deft touch of China’s policymakers:

China’s total debt reached 251 percent of gross domestic product as of June, up from 234 percent in 2013 and 160 percent in 2008, according to Standard Chartered Plc estimates.

Fortunately, they seem to have a firm grasp of their failings in this regard, and policy has been crafted this year with a clear objective of credit rationalisation: slow the overall rate of credit growth, hit shadow banking hard, and take the froth out of property prices. The great challenge of course is that China’s economy has grown hugely dependent on this model. As credit growth slows and questionable investment spending is restricted, the economy slows.

Along with the changes to mortgage rules in September, this interest rate cut sends a clear message that China’s authorities have become uncomfortable with the resulting hit to the economy from their credit tightening, and are prepared to tolerate looser conditions.

So, is this enough to fundamentally shift the outlook for the Middle Kingdom, and with it Australia’s?

I’m sceptical that this cut alone will be enough to reignite the credit binge necessary to produce a large upswing in activity, more likely it’s intended to help the economy glide towards slower growth rather than crash. And I wouldn’t be jumping to the conclusion that the government has abandoned its commitment to credit rationalisation. My view is that authorities are looking to place a floor under growth, rather than blow the roof off again.

I know I’ve said it a few times in the last couple of months, only to see the market cruelly mock my optimism, but I’ll try again anyway: I won’t be surprised if this move from the PBoC offer respite to our beleaguered iron ore miners by seeing off a new low in spot this year. By don’t expect a stomping rebound, since nothing has fundamentally changed in the market, and do expect a resumption of pain next year.

AUD has been heavily bid since the announcement, up about a cent against the USD, as have equities.