Part 1 – The Making of the Australian Triumph

I’m sure George Megalogenis, journalist and author The Australian Moment, was being sincere when he wrote:

Are we in danger of becoming a great country? When I put the question to politicians and officials in interviews for this book, the majority response is to laugh or sigh.

Be that as it may, just because Australian politicians and officials weren’t seized by a collective great power delusion doesn’t mean that Australian Exceptionalism was absent from our policymaking mindset; far from it. This sense of exceptionalism manifested itself in a constant tendency to overestimate the durability of the mining boom, which has lasted all the way through to the present day. While the Bureau of Resources and Energy Economics has traditionally been the main offender, the most risible delusion today belongs to the Western Australia government, which has forecast iron ore at $122 for 2014-15. So far iron ore has averaged $86 this financial year, and is currently sitting at $70/tonne. There’s been cascade of revisions to iron ore price forecasts lately, and Chinese futures are pricing spot at close to $60 by May next year. Plainly, the WA budget is in big trouble. Although federal budget forecasts have been less sanguine, Canberra is still facing an unpleasant shock; as I’ve argued since this blog’s inception, the public balance sheet is under far greater stress than is typically recognised, mainly because iron ore is in significantly more trouble than has typically been acknowledged (until very recently, of course, when the market made it impossible to deny).

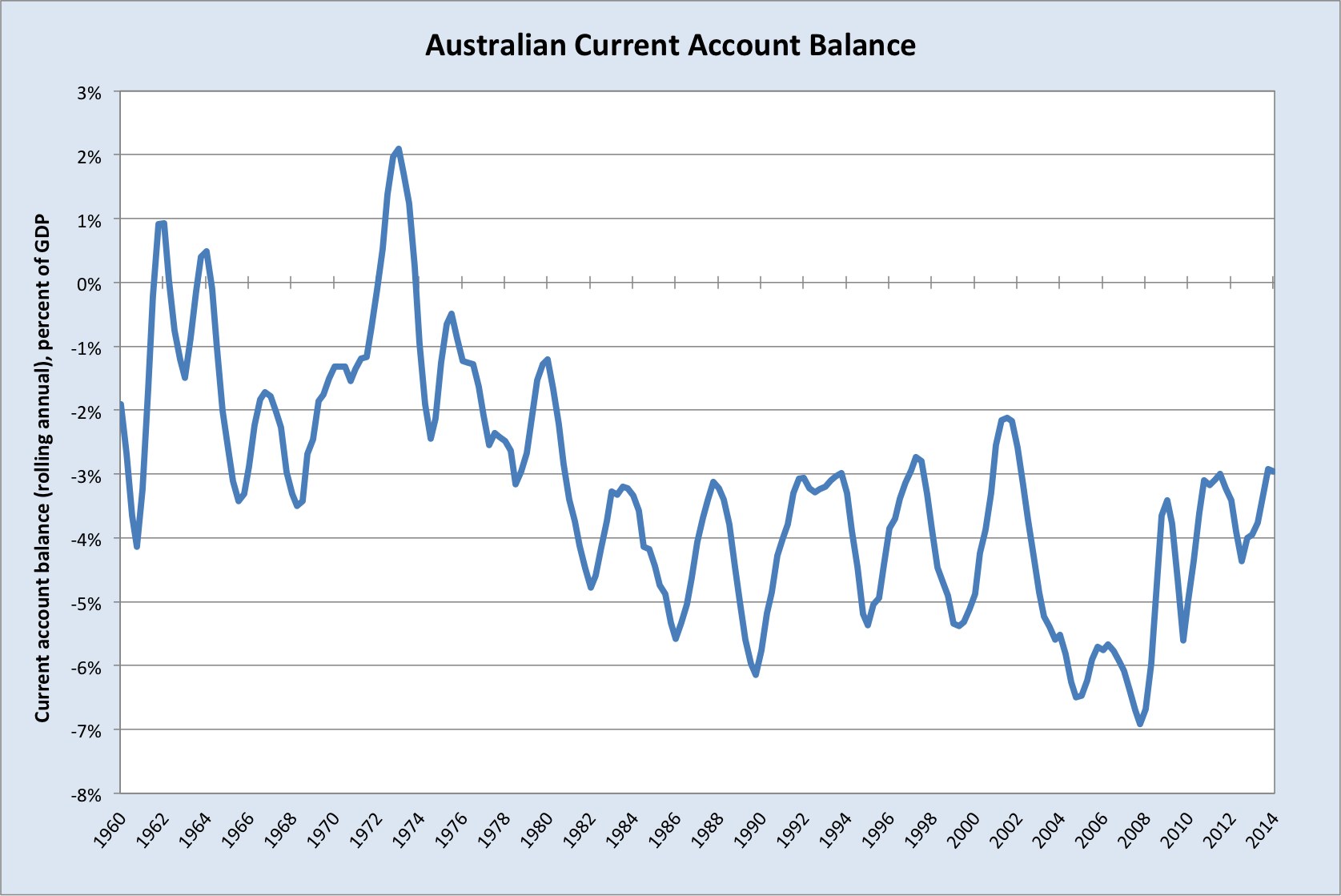

The idea that our prosperity would be underwritten by demand for our minerals and energy has had a pervasive effect on politics over the past decade, and led to what Professor Ross Garnaut dubbed the ‘Great Complacency’. This argument is a noticeable departure from the one advanced by Megalogenis, which I covered in the previous post. This is actually quite odd, seeing as he agrees with most of the particulars but arrives at a completely different conclusion. The thrust of the ‘Great Complacency’ argument is that there weren’t sufficient adjustments made to fiscal policy to reflect the transient nature of the terms of trade boom. We can see this plainly enough in the rather pathetic fact that we’ve reached the denouement of a huge mining boom with a federal budget mired in structural deficit and a current account deficit that never even threatened to close (the current account balance is the trade balance plus net foreign income).

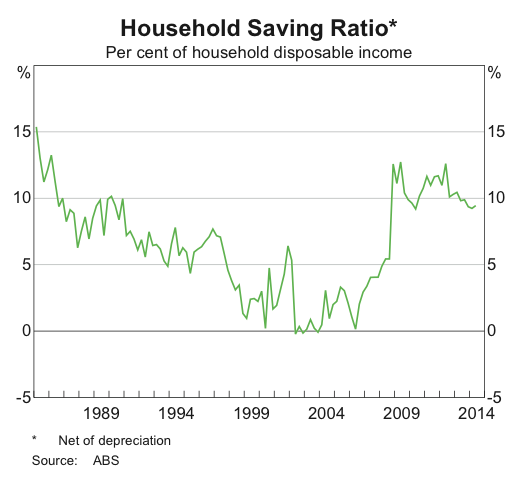

Worse than that, the initial phase of the terms of trade boom, prior to the financial crisis, saw some of the largest current account deficits of modern times, as Australian households threw aside the old art of saving in the new millennium.

This was the legacy of the housing frenzy, which peaked in 2003-04. It was also the period through which fiscal settings should have been much tighter, as corporate tax revenues started pouring in from the early stages of the boom. Alas, the Howard/Costello budgets were too generous, delivering tax cuts and expansions to various entitlement programs, which boosted overall spending in the economy.

The combination of spendthrift households (at least until 2006, when the saving ratio began to rise), and a government eager to feed the habit, left the RBA with the job of leaning against the boom.

This monetary tightening formed part a deliberate strategy for adjusting Australia’s economic settings in response to the terms of trade boom. There were basically three ways that Australian policymakers could have dealt with the boom: a) real exchange rate appreciation by domestic inflation, b) real exchange rate appreciation by currency appreciation, c) a forcible increase in national savings. (Or some combination of all three, of course.) Understanding which approach was adopted, why it was adopted, and what it entailed, helps us understand Australia’s current outlook.

Super-cycles

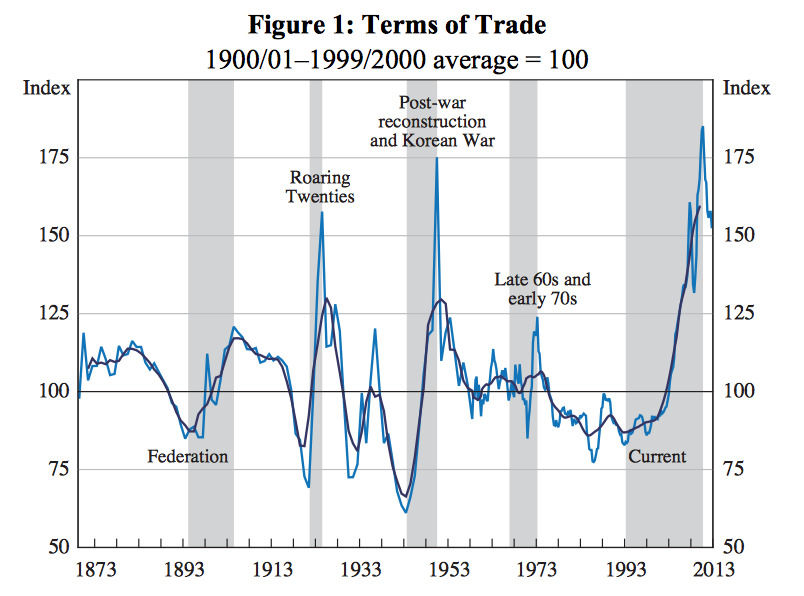

The boom Australia has just lived through is commonly referred as a commodity price super-cycle. Before I look at the a various ways of responding to the boom, this paper (fee required) by David S. Jacks has an excellent description of what we’re talking about when we refer to commodity price super-cycles (highlights my own):

In this paper as in others it follows, commodity price super-cycles are thought of as broad-based, medium-run cycles corresponding to upswings in commodity prices of roughly 10 to 35 years. These are demand-driven episodes closely linked to historical episodes of mass industrialization and urbanization which interact with acute capacity constraints in many product categories—in particular, energy, metals, and minerals—in order to generate above-trend real commodity prices for years, if not decades on end. Significantly, this paper finds that fully 15 of our 30 commodities are in the midst of super-cycles, evidencing above-trend real prices starting from 1994 to 1999. The common origin of these commodity price super-cycles in the late 1990s underlines an important theme of this paper: namely that much of the recent appreciation of real commodity prices simply represents a recovery from their multi-year—and in some instances, multi-decade—nadir around the year 2000. At the same time, the accumulated historical evidence on super-cycles suggests that the current super-cycles are likely at their peak and, thus, nearing the beginning of the end of above-trend real commodity prices in the affected categories.

Exactly what Australia has just gone through, in other words.

Plans A, B and C

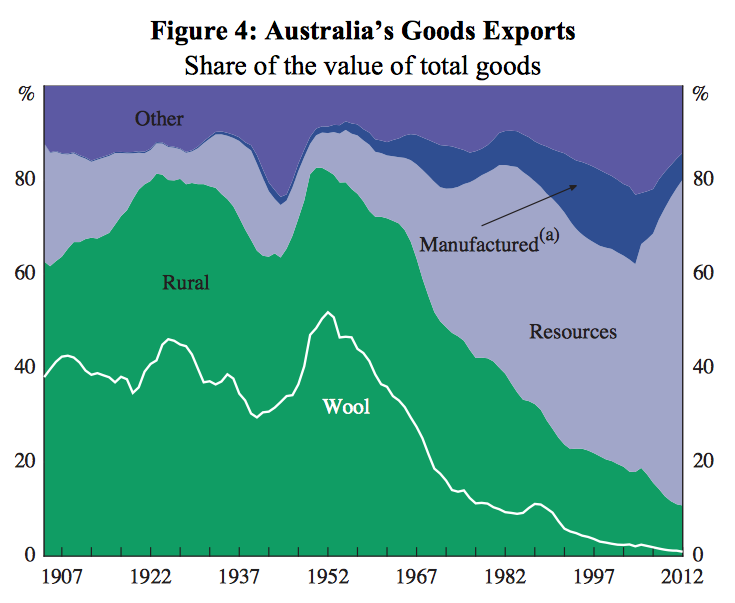

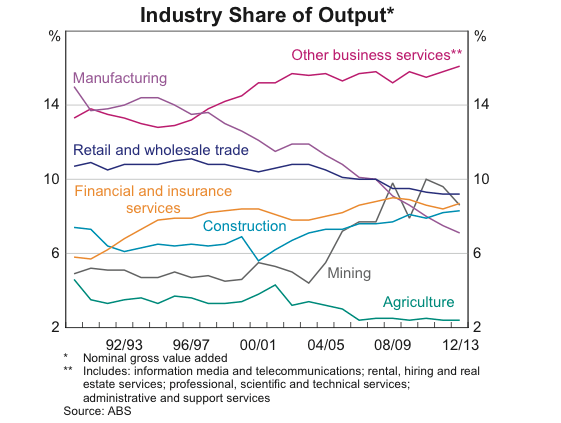

Primary resources account for the vast majority of Australia’s goods exports.

As a result, Australia has always been prone to commodity price boom and bust cycles.

Terms of trade booms entail a significant rise in Australia’s national income, since we’re able to exchange the goods we export for more (or higher value) imports. We get richer.

But most of us don’t sell iron ore on the world market, so how does the soaring iron ore price impact those of us who aren’t directly remunerated by the iron ore industry?

There are a few channels through which this can occur, but essentially it’s through an appreciation in the real exchange rate. The exchange rate that gets quoted to you when you travel overseas is the nominal exchange rate, which doesn’t necessarily tell us much about the relative purchasing power across different countries (think of nominal as ‘in name only’).

This point can be illustrated by way of a simple, stylised example: Suppose Australia’s nominal exchange rate is fixed against the US dollar at parity, but Australia has very high inflation, say 100% annually, whereas US inflation is zero. In a year’s time, you’ll (hopefully!) be getting twice as many Australian dollars in your pay check each week. The prices of haircuts and beers and electricity in Australia have also all doubled, so in real terms you’re no better off buying things in Australia. But you can still exchange each Aussie dollar (of which you now have twice as many) for one US dollar, since the rate is fixed at one-for-one. And since inflation is zero in the US, the prices of haircuts and beers and electricity haven’t changed at all. So if you exchange your Aussie dollars for US dollars, you can head over to the US and buy twice as much stuff! Despite there being no change the nominal exchange rate, Australia’s real exchange rate has appreciated.

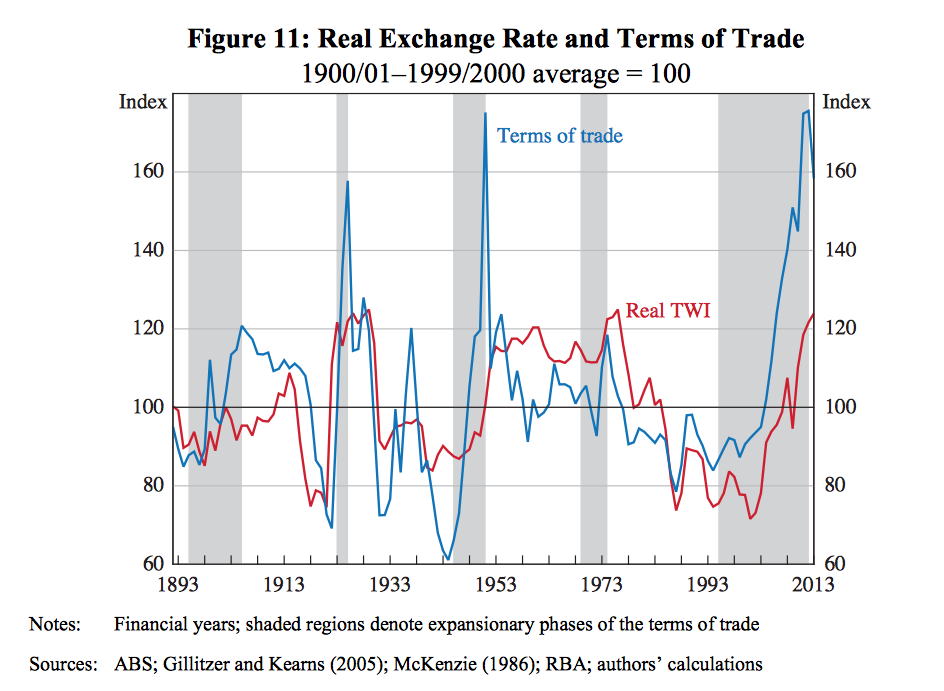

An appreciation in the real exchange rate has accompanied all of Australia’s terms of trade booms.

Here’s a close-up of the most recent boom:

When the terms of trade enters an upswing, additional income starts flowing into the economy, raising profits and salaries in affected industries and boosting government revenues. Unless the government purposely restricts spending by tightening the budget, this increase in income flows into the rest of the economy. Firms raise investment and households consume more. Until 1983, when Keating floated the dollar, Australia’s nominal exchange rate was fixed (well, tightly managed). If the nominal exchange rate is fixed, then there’s no automatic mechanism to make life harder for trade-exposed industries that are not directly benefiting from the terms for trade upswing, so firms aggressively compete for scarce labour, driving wages higher. As spending and income rises throughout the economy, inflation rises. Thus, as I described above, Australia’s real exchange rate rises.

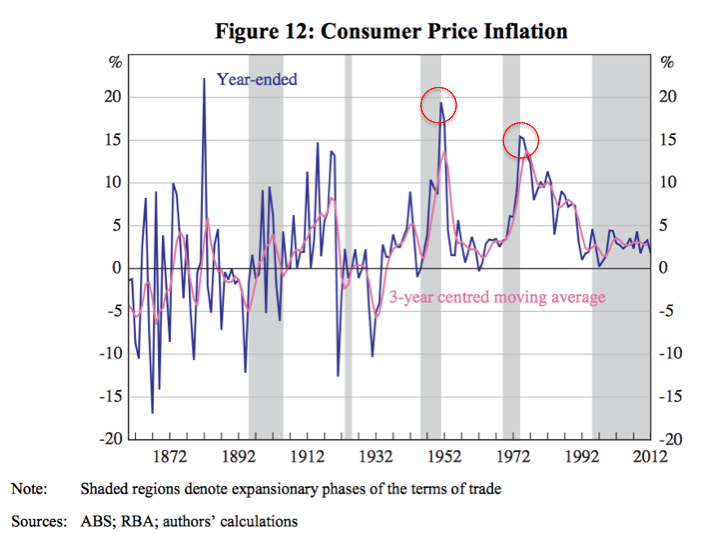

Although I’m not sure it was really anyone’s plan in the past, for convenience I’ll call this Plan A for responding to a terms of trade boom: permit domestic inflation to rise. The biggest problem with this is that it’s all well and good during an upswing, but it can be most damaging during the downturn, and typically entails a recession. The reason being that the economy has become uncompetitive at the new level of the real exchange rate. Returning to the Australia-US example above, if Australians can afford to buy more US-made beer than Australian-made beer, and they can since inflation is so high in Australia relative to the US, then they’ll shift their demand to US-beer. This behaviour is repeated for most other tradable goods, and so higher inflation hurts Australian businesses. When the positive effect of the terms of trade upswing abates, the now-uncompetitive economy cannot sustain full employment, and slips into recession. (Generally there was some belated monetary tightening to address rising inflation, and this would exacerbate the downturn when it arrived.)

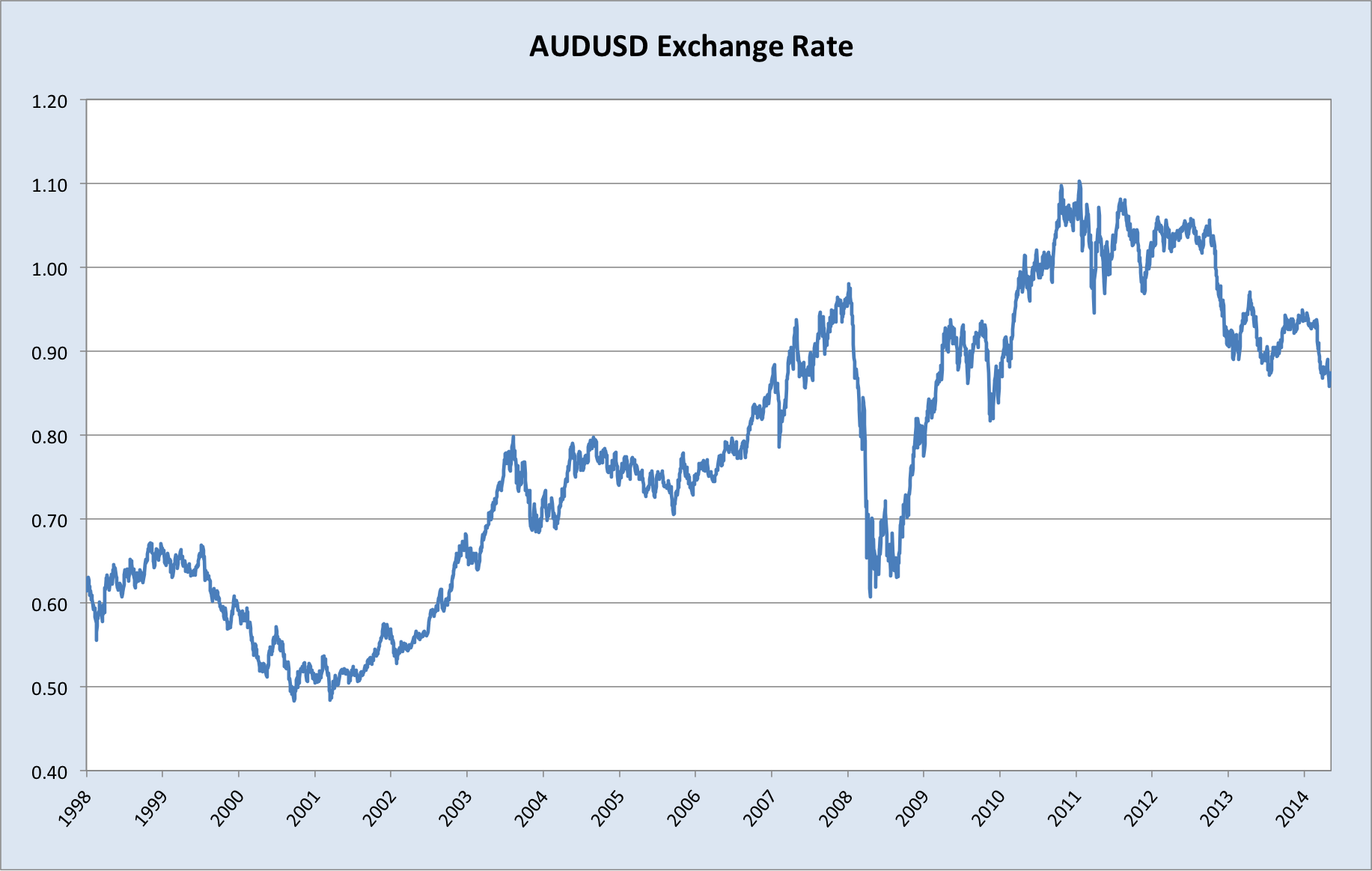

This is why it’s commonly agreed that one of the central achievements of the most recent terms of trade boom has been the prevention of an inflationary breakout (see CPI chart above for comparison to past booms). Instead, since it was accepted that the real exchange rate had to rise, the nominal exchange rate did the heavy-lifting, allowing inflation to remain in check (or ‘anchored’, in econospeak). That is, instead of the Australian dollar being fixed against other currencies, it traded freely, and rallied very strongly indeed.

In Macroeconomic Consequences of Terms of Trade Episodes, Past and Present (2014), Atkin et al had the following to say (p. 21):

Prior to the current terms of trade cycle, the RBA adopted an inflation-targeting framework, with the goal of keeping consumer inflation between 2 and 3 per cent on average over the medium term. This framework has provided a clear nominal anchor which, together with changes to the structure of the labour market described in Section 4.5, limited the feedback of the boom to economy-wide prices and wages. Notwithstanding the very significant rise in the terms of trade in the current episode, inflation has been well contained, especially when compared to the experience of the 1950s or 1970s. The floating exchange rate and inflation- targeting framework has also provided the RBA with the flexibility to maintain an accommodative stance of monetary policy more recently to support domestic demand since the terms of trade has started to fall.

And in an earlier RBA research paper, titled, The Mining Industry: From Bust to Boom (2011), Connolly and Orsmond had a similar take (p. 47):

Australia’s freely floating exchange rate has allowed a real appreciation to occur in response to the 2000s mining boom without the adjustment coming through high inflation, as occurred under the less flexible exchange rate regimes of the 1970s and early 1980s. The surge in mining export receipts in the late 1960s and early 1970s generated strong domestic demand and placed upward pressure on the exchange rate. The Government kept the exchange rate fixed, building foreign reserves and allowing the domestic money supply to grow at an annual rate of over 20 per cent in the early 1970s (Figure 25). When the Government finally revalued the exchange rate in late 1972 and 1973, it was too late to restrain inflation, which had drifted up from around 3 per cent in the late 1960s to 7 per cent in 1971. In contrast, during the 2000s, the floating exchange rate began appreciating as the global economy recovered from the 2001 recession, and appreciated further over the remainder of the decade as the terms of trade continued to rise. Furthermore, when commodity prices moved sharply in 2008/09, the exchange rate adjusted to cushion the shock to the economy. Overall, the higher exchange rate has helped to offset the expansionary effect of the increase in mining export receipts and investment.

I’ll call this Plan B: still allow the real exchange rate to rise in response to the terms of trade upswing, but keep inflation anchored, prevent a wage breakout, and leave it to the nominal exchange rate to rise and fall in accordance with the economy’s needs. This entails is a shrinking of various other tradable-goods sectors in the economy, which can’t compete internationally when the Aussie dollar is so strong, to ‘make room’ for the booming resource sectors. As the nominal exchange rate rises, Australians get richer in real terms and demand more imported goods, which are cheaper relative to locally-produced goods. Consequently, trade-exposed sectors and businesses which aren’t benefiting from the boom start to struggle; they reduce their demand off workers and curtail new investment. This process reduces inflationary pressures in the economy during the upswing.

What makes a nominal exchange rate appreciation so attractive is the comparative ease with which the economy will adjust to the downswing in the terms of trade, at least in theory. As the terms of trade decline, and drag down national income with it, the Australian dollar will lose value. As the Australian dollar loses value, sectors which were getting squeezed by the booming resource sector will see an improvement in demand for their products, and this will support business investment and employment.

So we’ve arrived at one of the fundamental points of the Australian economy today: With the terms of trade bust and the resource investment wind-down gathering pace, the Australian dollar must fall substantially from its current level. Most people I think probably appreciate this intuitively. However, we are talking about a very big adjustment indeed, 20-30% lower than where the Aussie dollar is trading presently, at least.

If this nominal exchange rate depreciation is not realized, if the Australian dollar does not lose value against the relevant currencies of trade partners and competitors over the next couple of years, unemployment will rise significantly. Of course, one way or another, it almost certainly will happen. It’s a matter of timing. The Aussie dollar will fall when it becomes clear than Australian interest rates are going a lot lower and most likely staying there for an extended period. Therefore, the longer the RBA waits, the worse the employment situation will get. But rising unemployment is itself one of the most important indicators watched by the RBA, so in that sense the bank will be forced to act sooner or later. Whether the board is proactive or reactive in this instance is the main question.

Sounds pretty simple, doesn’t it? All the Australian dollar needs to do is fall precipitously and the economy will be fine! Would that it were that easy.

Sadly the Australian case is complicated by the situation in the housing market. Although the economy needs lower rates to bash the currency (there are other options but the RBA is loath to countenance these), this action invariably provokes a rapid and destabilising response in the housing market. In the next post I’ll run through the challenge associated with the housing market, and why it complicates the real exchange rate adjustment.

Must we grow richer?

So far we’ve seen Plans A and B for responding to the terms of trade boom. Each entailed a significant real exchange rate appreciation, by domestic inflation and nominal exchange rate appreciation, respectively. But did the real exchange rate have to rise so strongly in response to the upswing in the terms of trade?

The current account balance is the difference between domestic demand for goods and services and domestic supply (you need to add in net foreign income earned in the period as well). As such, a country running a current account deficit is purchasing more goods and services than it is producing. To do so, it must borrow the difference from international lenders (or sell assets to international investors). A country that is borrowing more from than it is lending internationally, is running a capital account surplus. Together, the current and capital accounts make up the balance of payments.

One might be excused for assuming that Australia would have run significant current account surpluses during the biggest boom in exports in over a century. But in fact, as my chart above illustrates, at no stage during the boom did Australia notch up a surplus. Indeed, before the financial crisis in 2008, Australia’s current account deficit reached record highs.

This occurred by a combination of the rising real exchange rate and rising foreign borrowing. As the exchange rate rose, the cost of imports fell and households purchased more of them. There was also a significant increase in household leverage which began in the mid-1990s and continued through to 2008. After 2008, when households boosted savings out of current income (which lowered demand for imports), the trade balance sporadically swung into surplus, but owing to Australia’s substantial foreign liabilities, our net income on foreign investments is deeply negative, so the current account remained in deficit.

This failure to record current account surpluses and reduce Australia’s net foreign liabilities during the boom years leads some to complain that Australia squandered the boom. I count myself among this group. Current account deficits certainly aren’t intrinsically bad; if there’s an abundance of productive investment opportunities in your country but insufficient domestic capital or technological knowhow to exploit them, then importing foreign capital is sensible. But what net foreign liabilities mean is that part of the income generated in your economy each year must flow overseas in the form of interest and dividends. Therefore, large accumulated deficits are a drain on national income. They also leave the economy exposed to the availability of foreign capital, which can pose risks to the banking system.

I am of the view that the Australian government would have been better off running very big budget surpluses before the financial crisis, and parking these savings in an offshore sovereign wealth fund (whether this would’ve been politically feasible is another matter entirely). This would have been achieved by withholding almost all of the increase in additional revenues flowing from booming corporate tax receipts, which should have been further inflated by a pre-existing rent tax on resources. One consequence of this policy would have been lower household spending, including on imports, since tax cuts and middle-class entitlement spending fuelled consumption. With lower imports and booming exports, the current account deficit would have declined. In addition, lower household spending would have lessened the need for the RBA to raise interest rates as high as it did, which would have limited the appreciation in the real exchange rate. Again, this would have lowered spending on imports and eased the hit to non-mining trade-exposed sectors.

Had this policy been in place when the financial crisis arrived in 2008, the federal budget would have been in such healthy shape that subsequent deficits would have been far lower, and in fact the budget could have conceivably remained is surplus. This would have afforded the government far more breathing room to set stimulatory fiscal policy today.

This then is, or was, Plan C: Instead of allowing the real exchange rate to appreciate so strongly, irrespective of how it happens, lean heavily against the boom by running very big federal budget surpluses and reducing Australia’s net foreign liabilities. Some manifestation of Plan C was basically the alternative to Garnaut’s ‘Great Complacency’. In adopting this approach, comparatively subdued household spending acts as a release valve, mitigating the risk of the economy overheating. Contrast this with Plan B (real-by-nominal exchange rate appreciation), where it falls primarily upon the non-mining tradable-good sectors to shrink and so act as the release valve.

A rise in the real exchange rate would undoubtedly have been necessary, but by shifting the balance and leaning against household consumption and borrowing, Australia would have improved its foreign debt profile (the net international investment position), its public finances would have been in much better health, and there would have been less hollowing out of tradable-goods sectors as a result of the boom.

We can’t fully judge Plan B until we’ve seen how the economy performs in the bust, which is presently unfolding. The key question is, will non-mining business investment and hiring rise quickly enough to offset the mining bust? It may yet do so, though the chances seem fairly slim. In my eyes, a greater emphasis on Plan C would appear to have been best option for the nation. Hopefully there’s another once-in-a-century terms of trade boom before too long so we can test that hypothesis!