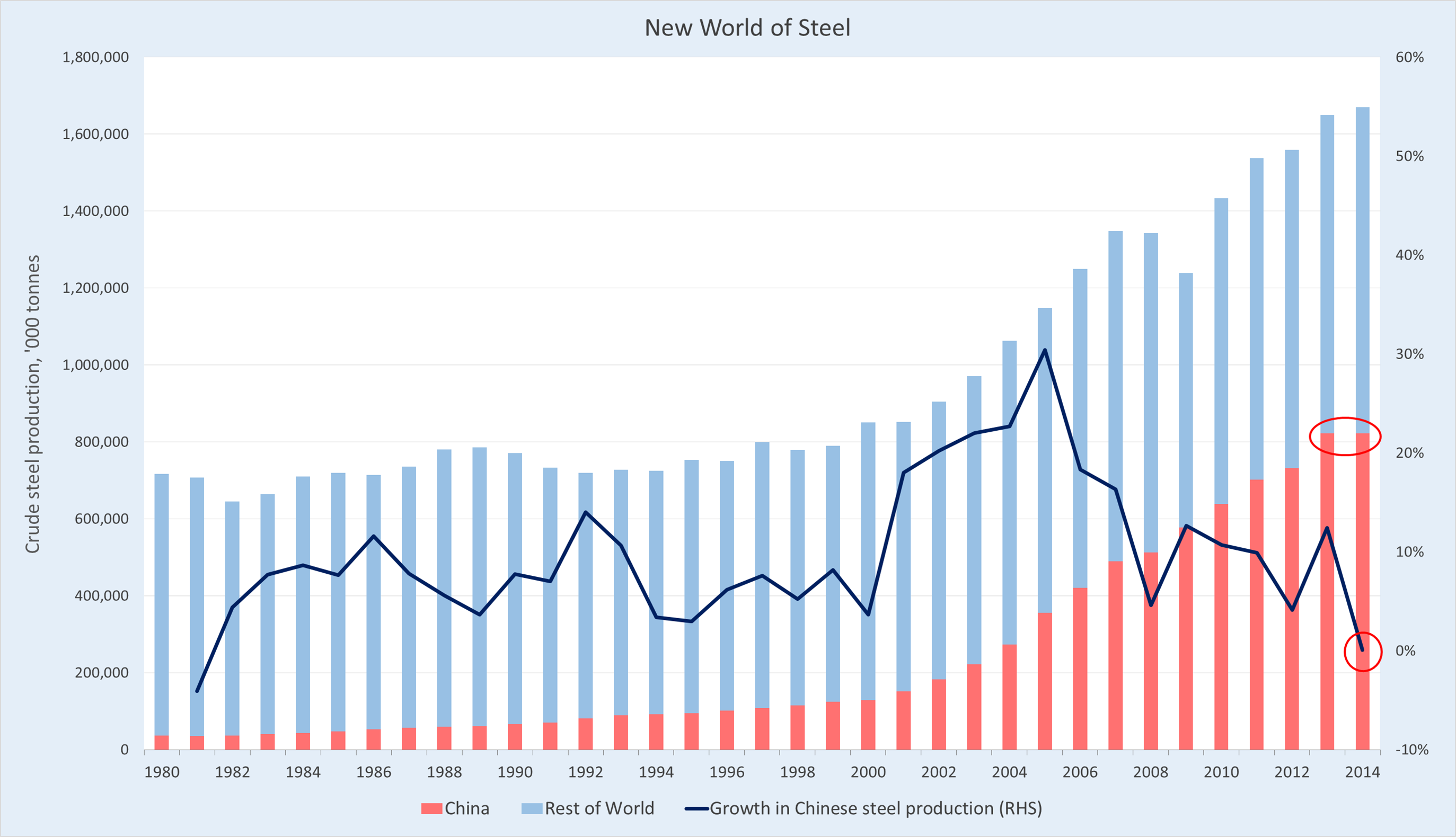

Since the turn of the millennium, as the composition of Chinese demand became increasingly dominated by state-directed investment spending, China has accounted for roughly 85% of the increase in world steel output. In nominal terms, this drove Australia’s iron ore export earnings up 15-fold between 2004 and 2014.

This boom has peaked, and indeed, as I pointed out a number of times last year, current levels of steel production in China are only being supported by strong growth in exports; domestic consumption actually declined 3.4% last year, to 738.3 million tonnes.

Although the growth in Chinese steel demand has crested (unless the government decides to reverse its policy stance and announces a big stimulus program), I also see little chance of it falling precipitously in the near future. But this lack of growth in output still presents a big challenge. We simply aren’t going to see the billion tonnes of annual Chinese steel demand by the end of the decade that was conventional wisdom until very recently. This means that iron ore producers are fighting over a shrinking pie and iron ore prices will continue to slide, I would say for another two years at least.