When I started this blog, I was well aware that its dominant theme was to be the stark divergence emerging between key sectors in the Australian economy: On one hand, the terms of trade were crashing, declining resource investment was primed to rip a hole in domestic expenditure, and Australia’s poor international competitiveness was inhibiting the revival of investment in non-resource tradable industries. On the other hand, we had the cyclical upswing centred on the Sydney and Melbourne property sectors, which policymakers hoped would boost consumer spending and employment growth. Whichever sector gained the upper hand in the short-term, I argued, would determine the next move in interest rates.

As we know, the army of professional forecasters was wrong; the RBA cut interest rates in February this year. Partially as a result of this, the sectoral divergence in the Australian economy has reached truly deformed levels of late.

I say partially for a couple of reason. Firstly, Australia’s external shock has gathered pace quicker than I anticipated (and as anyone who’s read this blog can attest, I’m about as bearish as they come on Australia’s terms of trade outlook!) The relentless slide in iron ore and coal prices (iron ore especially, of course), has hit national income hard and added urgency to the miners’ cost-cutting drive, which directly reduces household income. Furthermore, the oil price bust has hammered the economics of Australia’s gold-plated LNG projects, and ushered in a new emphasis on austerity in that sector as well. These trends are exacerbating the divergence in the economy on the structural side, and are obviously unaffected by Australian monetary policy.

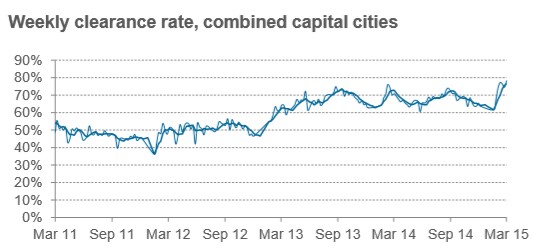

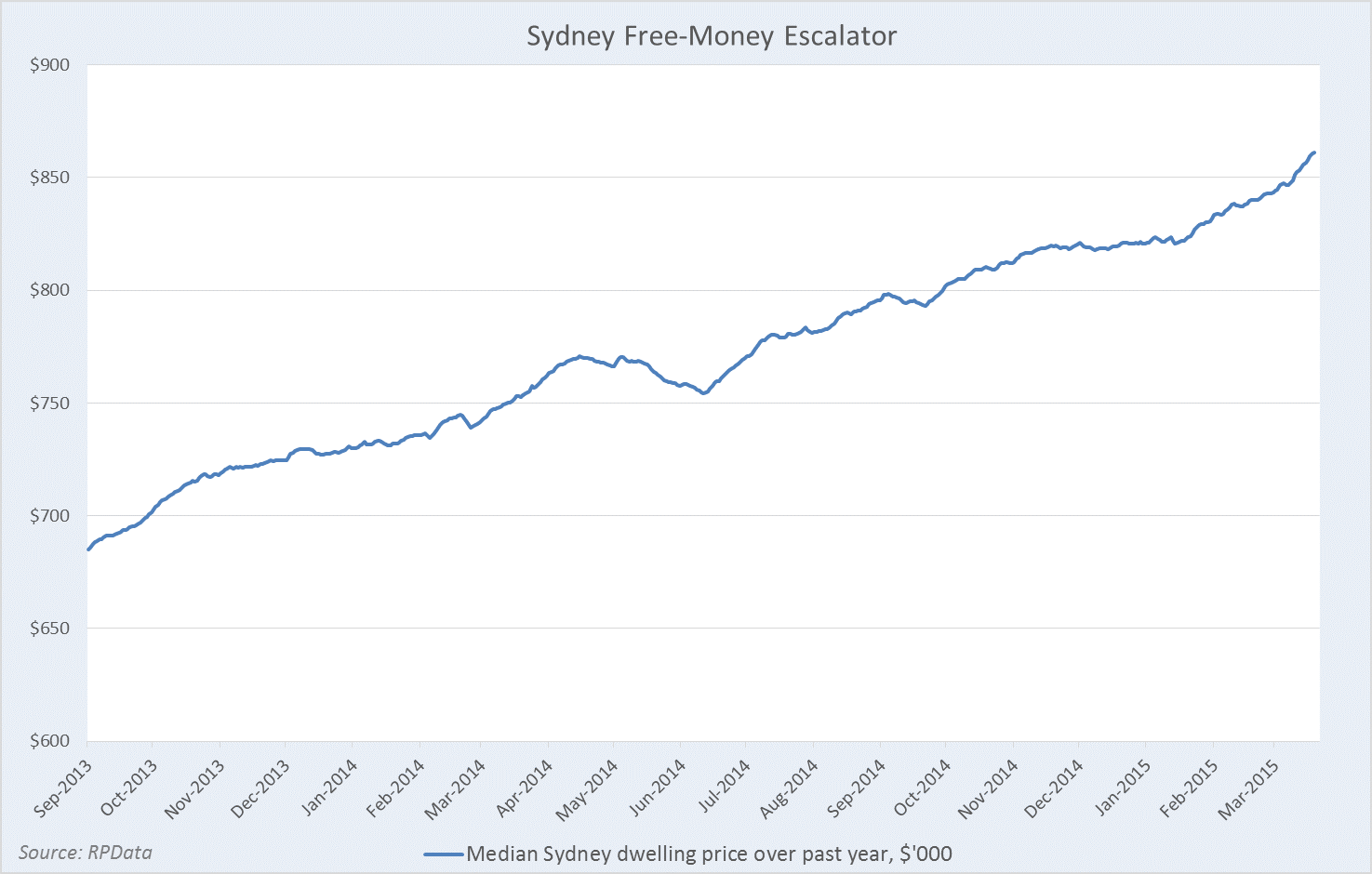

Moving in the other direction with disquieting rapidity is the boom in the East Coast property markets, Sydney’s in particular, which has shifted into a higher gear following the latest stimulus from the RBA. Pick any measure you like; Sydney property is white hot. Auction clearances have soared, investors are increasingly dominating new mortgage issuance, and price growth has rebounded to around 14% from a year earlier.

The property boom on the East Coast is undoubtedly being juiced by lower interest rates. But I believe it is incomplete to assign more than partial responsibility to the blunt tool that is the RBA’s cash rate.

The economy needed low interest rates, and it needs lower ones still,mainly to further reduce the value of the Australia dollar. As national income recedes with the terms of trade, and as resource investment winds down, unemployment will rise sharply unless we can revive activity in non-mining tradable sectors. This is not a lazy ‘competitive devaluation’: Australia had a very strong currency during the boom, and now that the boom has passed it is imperative that the value of the currency falls to match our lower national income and support employment. (Recent falls against the USD are welcome but on a broader basis, particularly against other commodity currencies, there is work to be done.)

So interest rates had to fall to reduce the value of the Australian dollar and repair our international competitiveness, but in so doing they’ve stoked a dangerous boom in property prices (which, incidentally, is a drain on productivity and so worsens our international competitiveness).

To overcome this apparent paradox, the RBA, in tandem with APRA, should have implemented regulatory controls to stifle speculative mortgage lending, especially when funded by offshore borrowings, before embarking on the latest easing cycle. That they did not, so soon after property bubbles ripped apart numerous developed economies, is a blemish on Australia’s economic policymakers. That they were dismissive of such options well into the boom is a serious indictment. That they finally started talking about macroprudential tools 6 months ago, was something of a relief… And that they still haven’t implemented the mooted controls with any bite, at such an advanced stage of the boom, is frankly an extraordinary failure.

Not only has this failure to act sowed systemic risks into the economy at about the worst possible moment, it is also seriously hindering the restoration of Australia’s international competitiveness; there are now strong indications that the RBA will have to hold off cutting interest rates for fear of fueling the rampaging property leviathan. From Peter Martin this on Friday:

Concern about the Sydney property market is shaping as an impediment to another interest rate cut at the Reserve Bank board’s next meeting in April, encouraging it to postpone the decision until May, a week before the federal budget.

A month of two more with an extra 25bps on the cash rate is not going to rein in the investor frenzy. Only rate hikes or a tough macpru regime has only prospect of success. Does the RBA want to sacrifice the wider productive economy to calm the passions of a property investors, or would be it preferable to slap tough, targeted regulatory impediments on the industry and carry on with the post-boom adjustment of lower rates and a lower Aussie dollar?