Aussie wilts along with the rest

A fortnight ago, I wrote:

As long as it’s relatively lucrative to borrow offshore and hold short-term AUD-denomiated assets, we aren’t likely to see a sustained fall in our currency.

This was quite unfortunate timing for me, given that I have been among the biggest AUD bears going around for the past 3 years. I hadn’t abandoned this conviction at the time of that post, but rather I was anticipating the Fed remaining relatively dovish; enough so that it wouldn’t send the AUD sharply lower until the RBA finally signalled the return of an easing bias. Whatever it was that fixed the market’s attention on the USD (those working papers from the Fed undoubtedly played a part), the timing of the AUD fall was plainly brought dramatically forward as the USD regained it’s mojo over the last fortnight.

I discussed the capitulation of the AUDUSD last week. Here’s how it looks today.

Chart from IG Markets

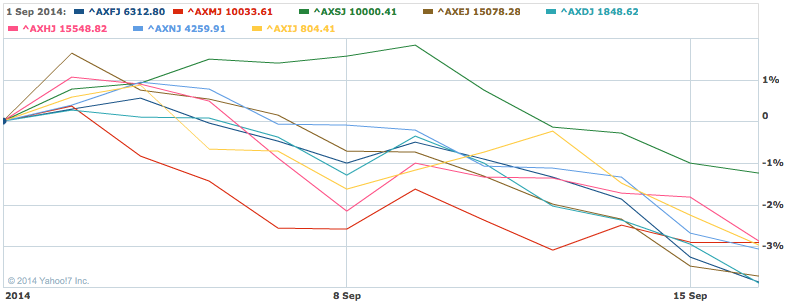

The mood in Australia is turning noticeably negative now. The local bourse has copped a hiding this month, down around 4% despite resilience in US equities.

The selling has been broad-based across sectors, however financials (XFJ), consumer discretionary (XDJ) and energy (XEJ) have led the charge, with materials (XMJ) continuing to languish due to the rout in iron ore. It’s worth remembering that financials and materials together account for half the local share market.

Chart courtesy of Yahoo Finance

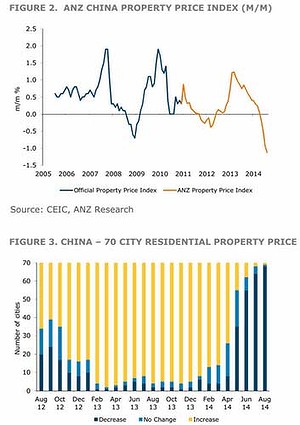

Weighing on sentiment towards Australia has been a poor run of data from China, beginning on the weekend. There have been short-lived bursts of excitement about government stimulus measures, but anyone hoping for a concentrated campaign to rescues fixed asset investment (and in so doing, rescue Australia), looks destined for disappointment. Rebar futures are again on the nose today.

Data on Chinese property were released today, and the downturn is carrying on with scant regard for the apparent imminency of stimulus.

It’s getting quite nasty now, and I expect property will begin testing the government’s reform fortitude in earnest in the coming months. As the Premier recently noted, it’s employment growth that is chief first among the government’s policy objectives. As long as employment is holding up, the government will tolerate deflating property. But what happens if employment starts to seriously suffer as a result of weakening property?

Australian asset allocation

As I said, despite an unfortunately-timed assertion that the AUD would be unlikely to decline materially (that is, break support at .9200), I have been and remain a long-term AUD bear. As such, I continue to favour stocks with a sizeable portion of earnings being generated offshore, or those with solid growth prospects for offshore earnings. This excludes the miners, however, since my bearish medium term view of their main product is central to my expectations for a lower AUD.

Candidates include Seek.com (SEK), CSL (CSL), Cochlear (COH), Westfield (WDC), Computershare (CPU), ResMed (RMD).

I’ve also liked Billabong (BBG) and Elders (ELD) and speculative plays for a while. Both have been crucified and are in the throes of restructuring. ELD is moving back towards a pure-play agribusiness model after various diversification disasters over the years. I believe there is long-term value in the strategy; if it can pull off the turnaround in its corporate model it will be well poised to take advantage of a lower dollar boosting Australia’s agricultural export sectors.

All advice is general in nature and does not take into account an individual’s circumstances. Proceed with caution.