On May 22 last year, Chairman Ben Bernanke announced that the Fed was preparing to reduce its purchases of US Treasury bonds and mortgage-backed securities (quantitative easing). The Fed is fond of coining new lingo for its activities, and the term it chose in this case was ‘taper’.

The bond market was not impressed.

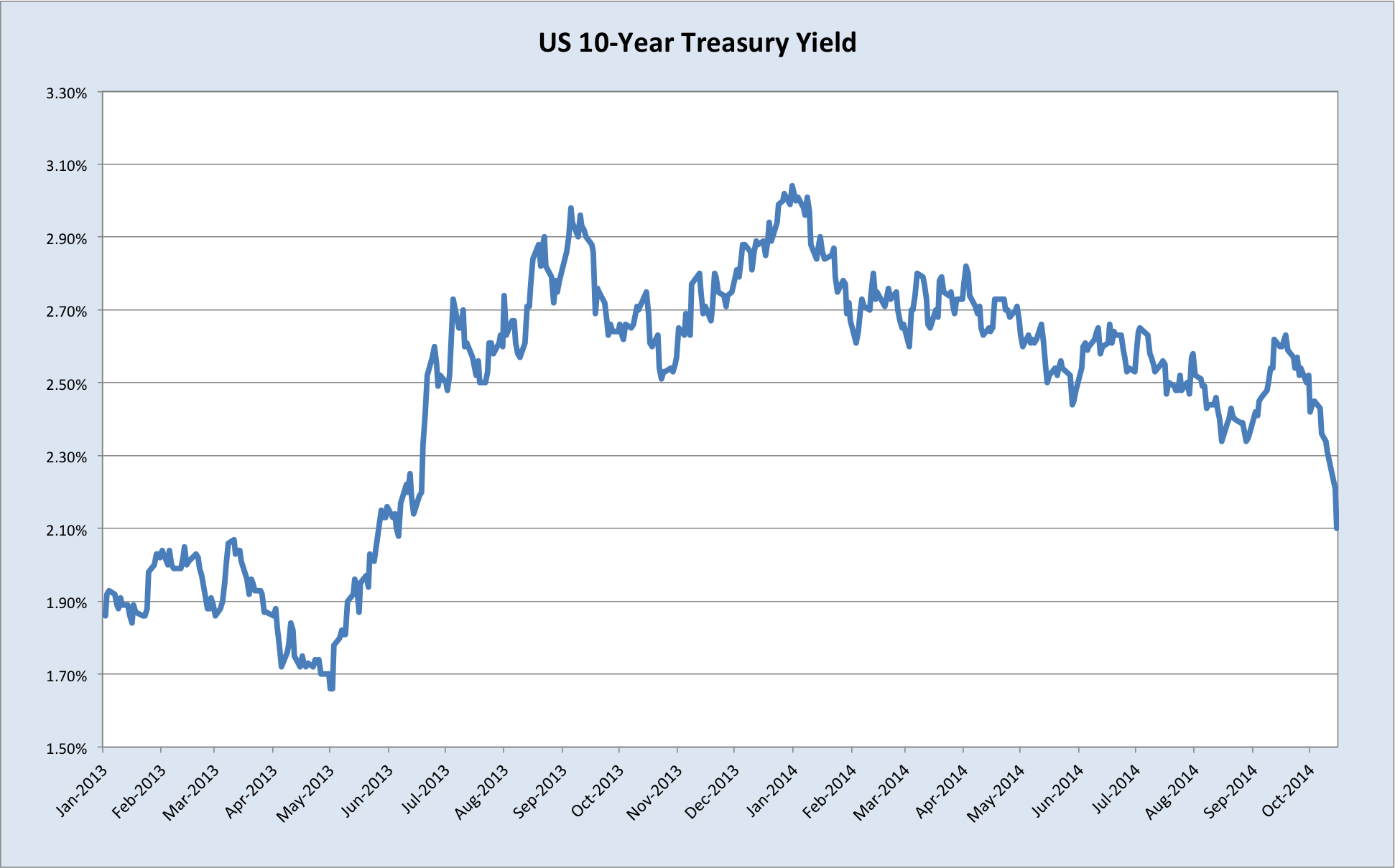

Having spiked off a low in early May, 10-year yields rose to be over 100bps higher by the end of June. The S&P500 lost around 7.5% over the same period, however this was a mere blip in the hefty rally of 2013. This episode is came to be regarded as the markets’ ‘taper tantrum’. With the dread-inducing end of QE now upon us, markets are growing similarly stroppy.

I devoted the lion’s share of my post on Friday to the heightened level of volatility ramming its way into global markets. Since then it’s been nothing but vol.

The CBOE VIX is a measure of the expected volatility of the S&P500 over the next 30 days. It’s now at its highest level since June 2012 (it briefly soared to over 30 last night, more on that in a moment). This was around the time that the liquidity-crisis phase of the European debt saga was concluded courtesy of Mario Draghi’s promise to do ‘whatever it takes’ to prevent a member state government from defaulting (meaning the ECB would buy as many sovereign bonds as was required to stem a meltdown). Until the last month or so, the VIX had been trending downwards thenceforth, which was both indicative and encouraging of risk-taking.

Much of this latest spike in volatility is attributable to the end of the Federal Reserve’s balance sheet expansion, however the timing is as much to blame, coming as it is when global growth expectations are taking a battering.

QE4?

Over the weekend a thought began to creep into my mind that I must confess I’d given barely a moment’s consideration to up until that point: What if the Fed isn’t done with its asset purchases just yet? What if we get QE4 or an extension of QE3?

I’m sure others more bearish than I have long been alert to this possibility, however I think it’s fair to say that recent data on the US economy, especially the labour market, have pointed to a steady healing. Not a roaring boom, by any measure; wage and other price pressures have been scant, but in all it looked like the US was on the right highway, albeit in a slow lane. Thus I had the following to say regarding the strong dollar:

The case for a stronger dollar has therefore centred on the miserable state of its peers. Germany is sinking into recession, adding to the persistent weakness plaguing the Eurozone, Japan is looking sickly after hiking the sales tax earlier this year, and China is doing its best to rebalance without detonating its debt time-bomb. Combined with the end of QE this month, the USD is looking the least ugly out of a pretty ordinary bunch.

Sadly, last night the US took a few steps closer to its miserable peers, with retail sales missing badly, registering the first negative print since the polar vortex froze activity in January, the Empire State Manufacturing Index falling back to Earth, and producer prices also in negative territory. I was surprised by the weakness in retail sales, I will admit, though the soft PPI shouldn’t come as a great surprise, when we consider recent developments in commodities.

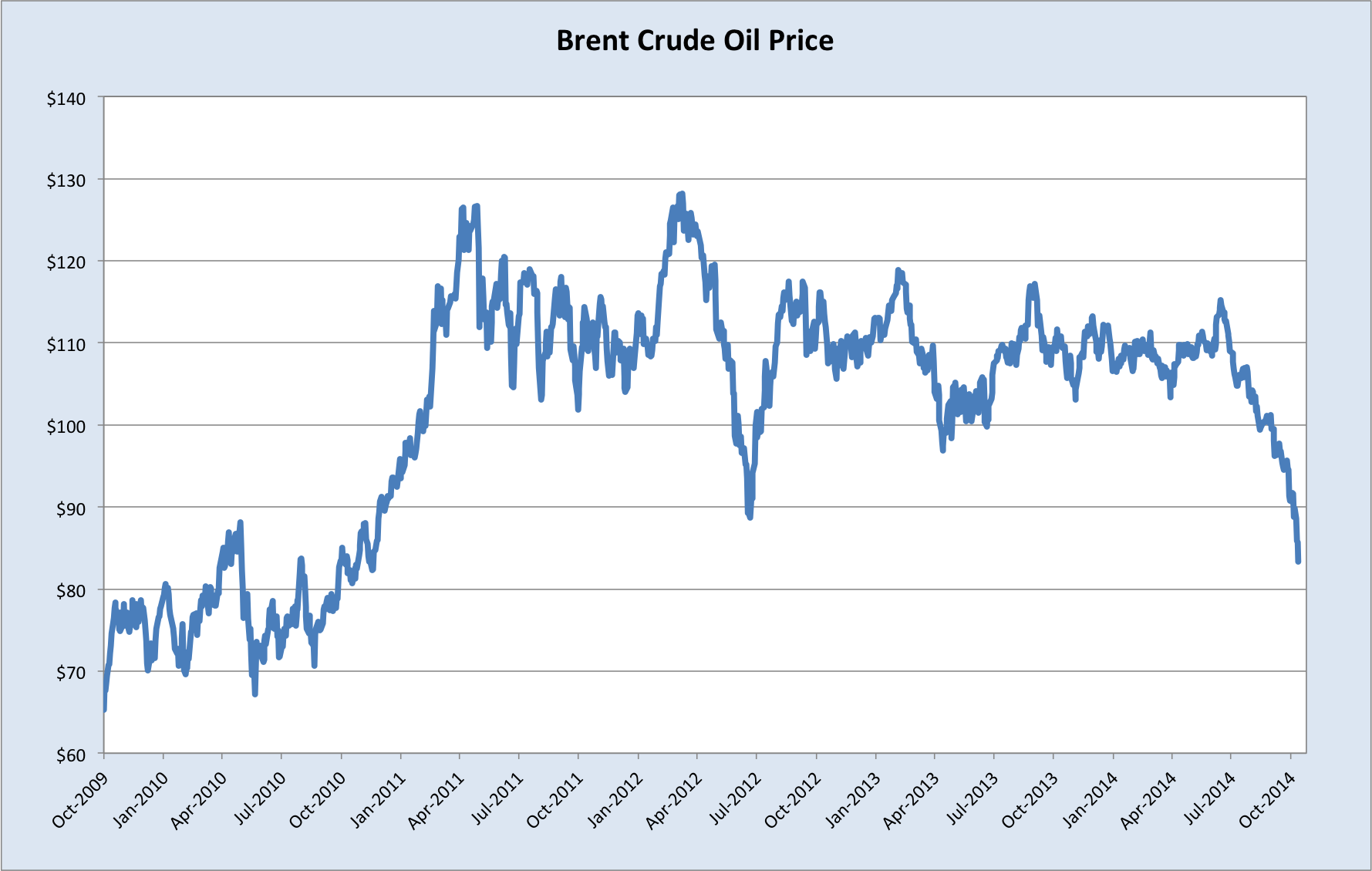

Along with rising volatility, another major theme I discussed on Friday was the slump in oil prices. (Here’s a useful recap of the reasons why this is happening.) Oil has been pummelled again this week, and is now down a jaw-dropping 27% since mid-June, to its lowest level in 4 years (and, it must be said, looking thoroughly oversold).

This pattern is being repeated across the commodity space, with the Thomson-Reuters CRB Index also nose-diving over the same period (oil and gas make up a large share of that index, it should be noted).

The sharp drop in commodities is draining price pressures out of the global economy at a rapid clip. Some of the recent drop is undoubtedly due to the USD rally. Nevertheless, from the US to the UK to China to Japan to Europe and even Australia, the spectre of deflation looms large over the global economy.

It’s beyond the scope of this post to delve into the possible explanations for this phenomenon, but suffice it to say, short of some radical shifts like a big cut to OPEC oil production or consumption-driven trade deficits in China or a credit boom in the US, I believe this phenomenon is likely to persist. The market agrees, and this is why US bonds have been soaring lately, and yields collapsing (see above chart), as expectations for US rate hikes are deferred.

Last night’s price action in equities was similarly informative.

Look at the enormous intraday volatility in that last candle, which saw the VIX briefly breach 30. A move like that suggests the equities market is extremely jittery but also still heavily imbued with the belief that the Fed will not hesitate to lend the support of its balance sheet if conditions deteriorate.

The USD sold off sharply, before recovering somewhat.

And gold caught a nice bid amongst the turmoil, helped as it always is by lower yields and a lower USD.

On Friday I highlighted the neat triple bottom that spot gold as put in. Although, at the time I said I was unconvinced that this would herald a sustained rally, as one may well be inclined to think it would looking at the chart. It’s now looking firmer, and this week’s movements in bonds make it much harder to see that support giving way in the near future.

So, QE4?

It has to be said that I didn’t expect last night’s data to be as bad as it was, nor that US yields would collapse this week in the manner they have. Nevertheless, one night of poor data of course does not mean that the wheels are falling off the slow but steady US recovery; it merely reinforces my view that “the US is looking the least ugly out of a pretty ordinary bunch”, as opposed to being in a robust upswing.

At this stage I find it far more likely that the Fed will simply defer its rate hikes, in preference to further asset purchases. But a fortnight ago I would have attached effectively zero probability to another round of asset purchases. Now I see somewhere between a 5-10% chance. And it’s not just me… John Williams of the San Francisco Federal Reserve conceded recently that if inflation remains low or declines further, another round of asset purchases is not out of the question.

Much therefore depends on how commodities fair and how soft things get in China, Japan and especially Europe. If inflation keeps wilting in these regions, and especially if the USD continues to rally, then the US will be importing disinflationary pressures regardless of whether its tepid recovery continues unimpeded. The Fed’s inclination to renew its asset purchases would come very quickly in that scenario.