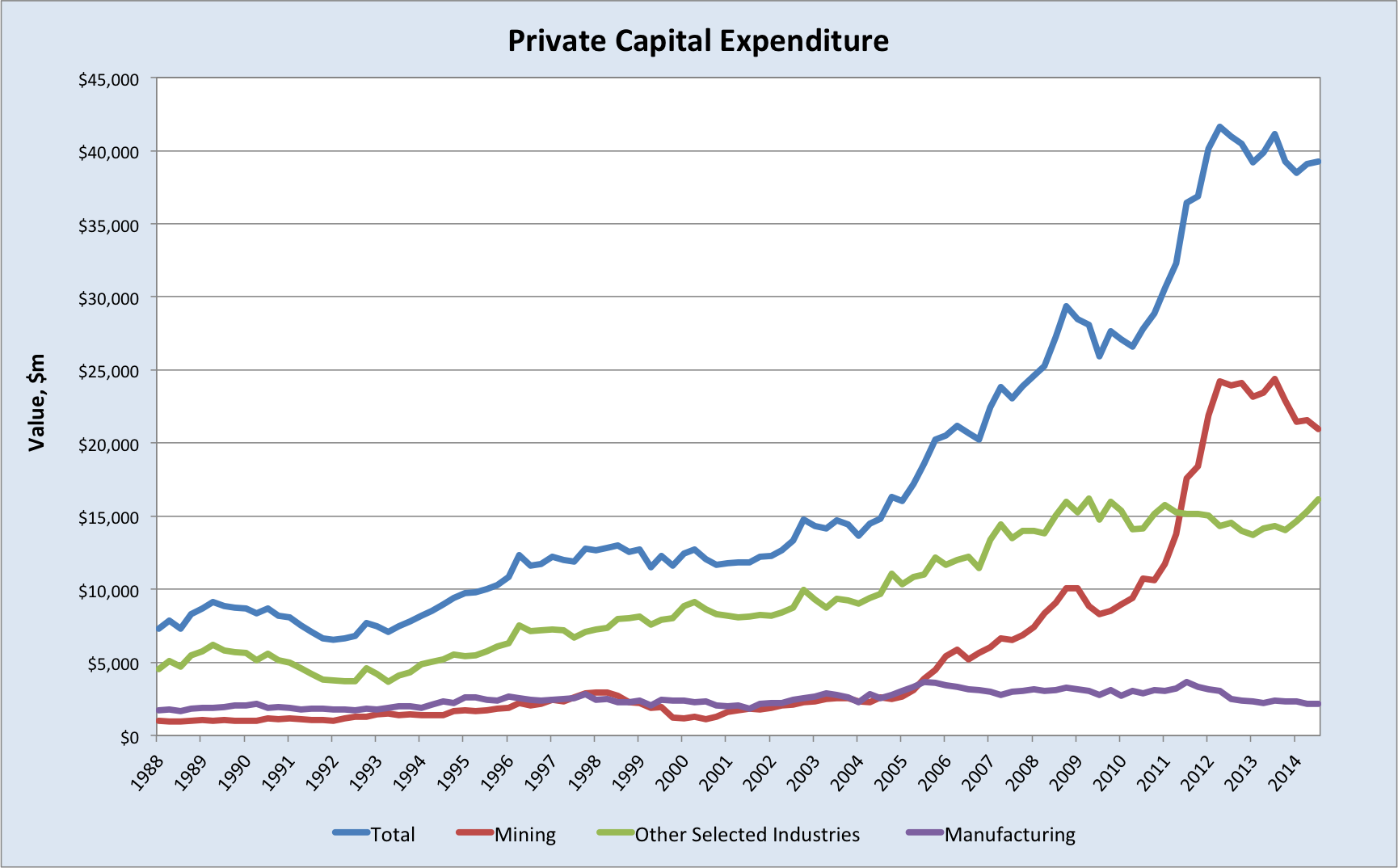

The results of the private capital expenditure survey for the September quarter were released by the ABS this morning, showing a seasonally-adjusted .2% rise, in volume terms, on the June quarter. This solidly beat expectations for a 1.9% drop.

In dollar terms, capital spending by the mining sector dropped 3% over the quarter and manufacturing fell 1.3%, with these falls offset by a 5.6% jump in ‘other selected industries’. Total capital spending was down 4.6% ($1894m) on the same quarter last year, mining was -14.2% ($3475m), manufacturing -10.5% ($253m), and ‘other selected industries’ +12.8% ($1833m).

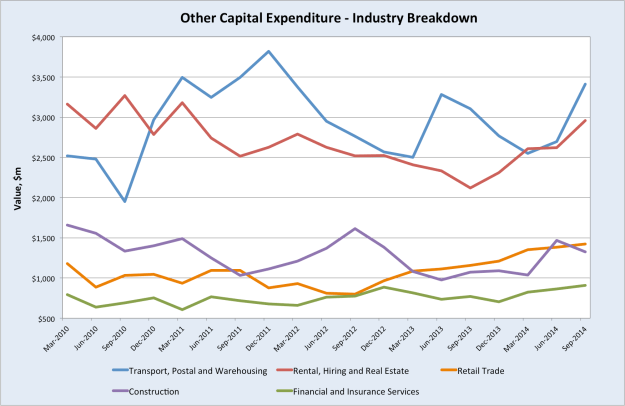

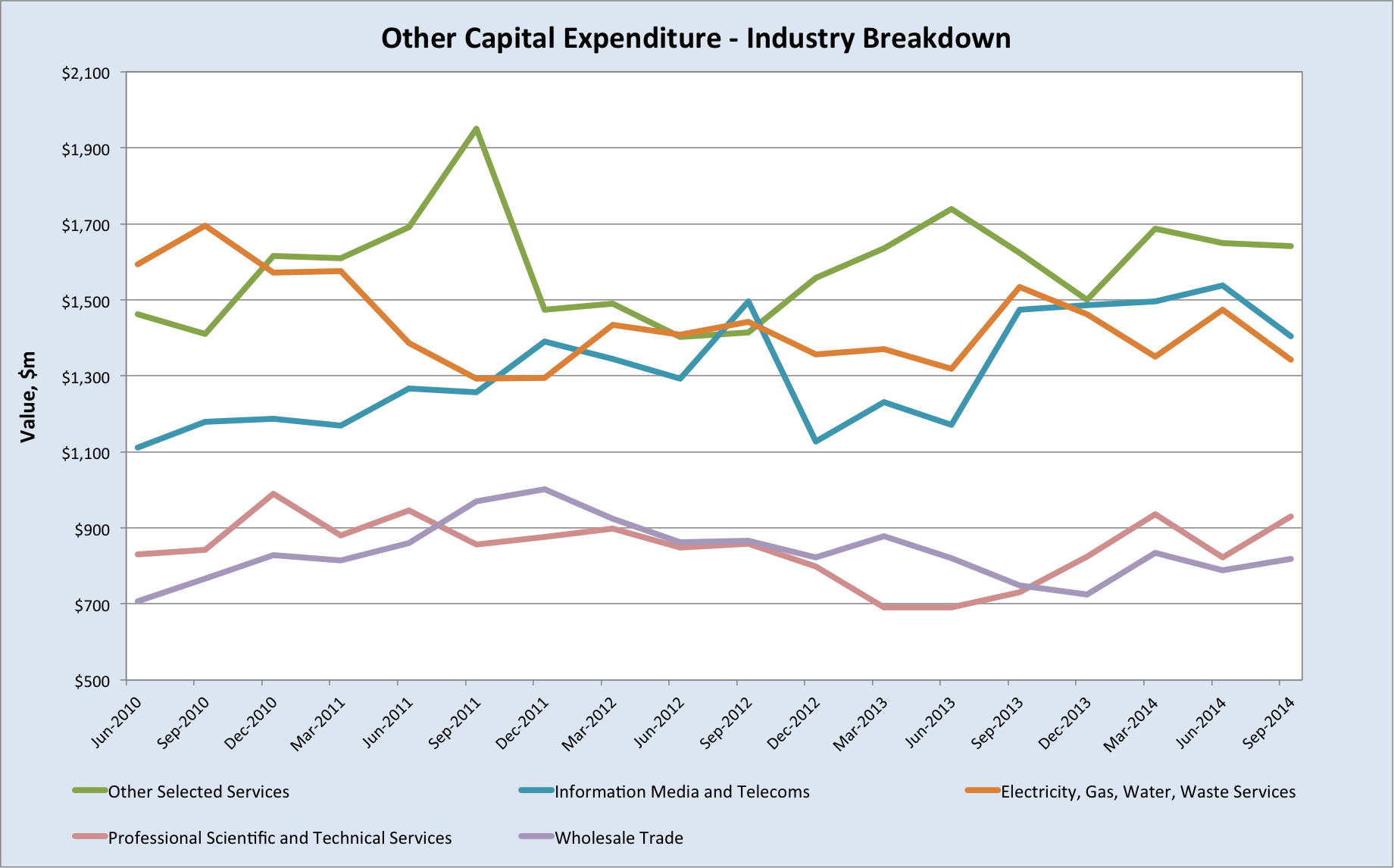

The main driver of capital spending by ‘other selected industries’ over the past year has been the ‘rental, hiring and real estate services’ industry grouping, which has risen by 40% and contributed $838m of the $1833m in additional spending by that sector. Contributions have also been made by businesses in ‘retail trade’, ‘construction’ and ‘financial and insurance services’.

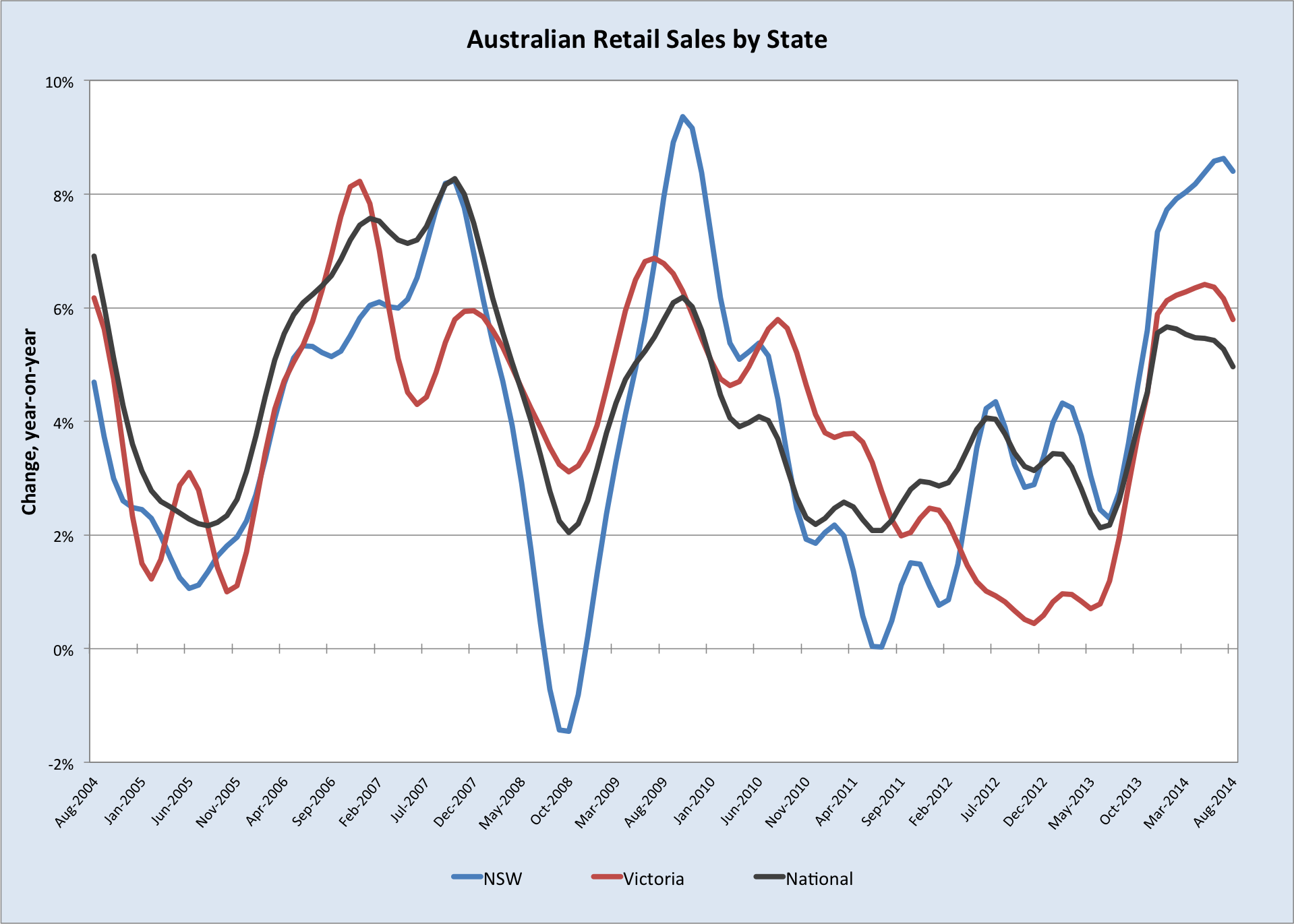

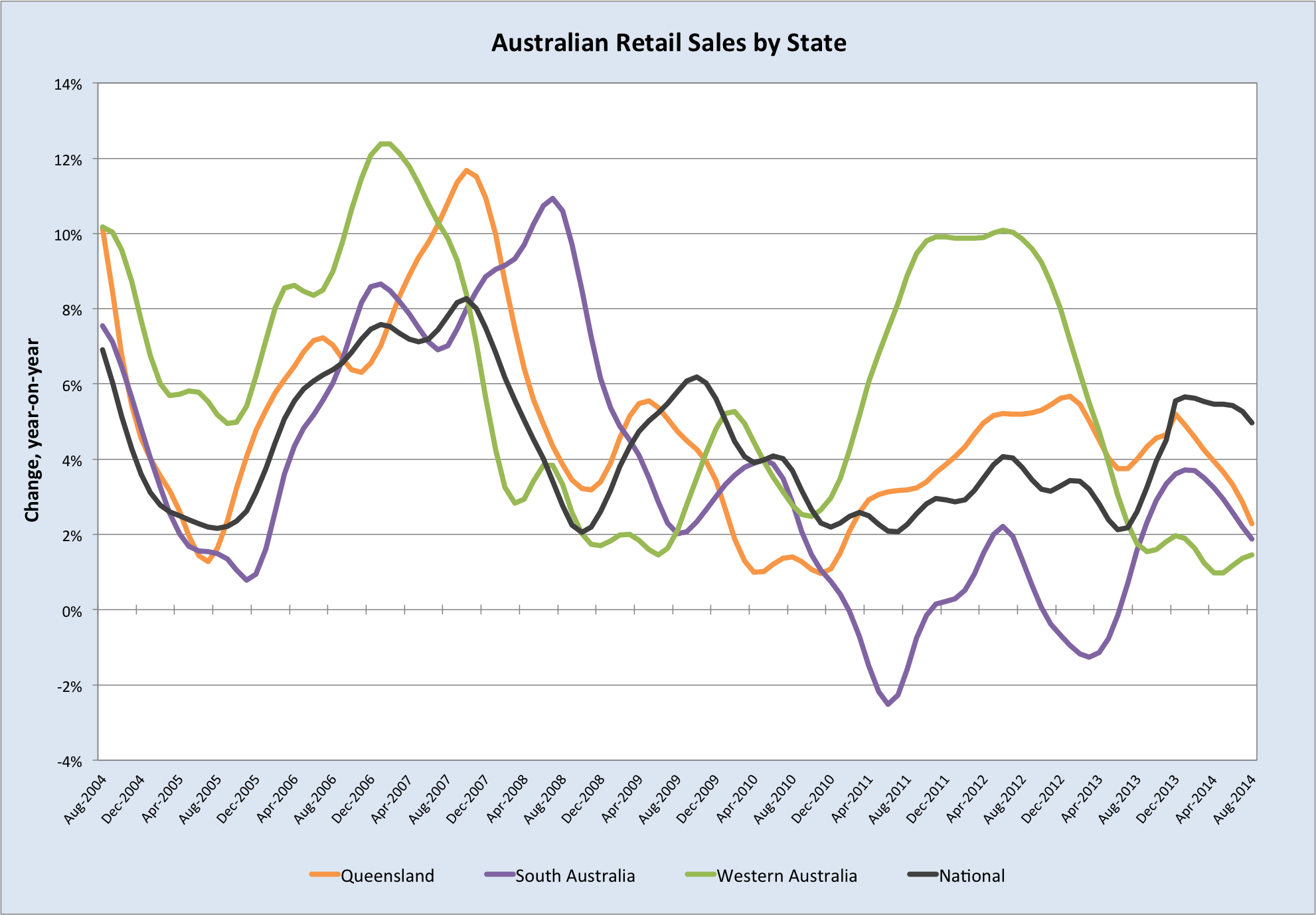

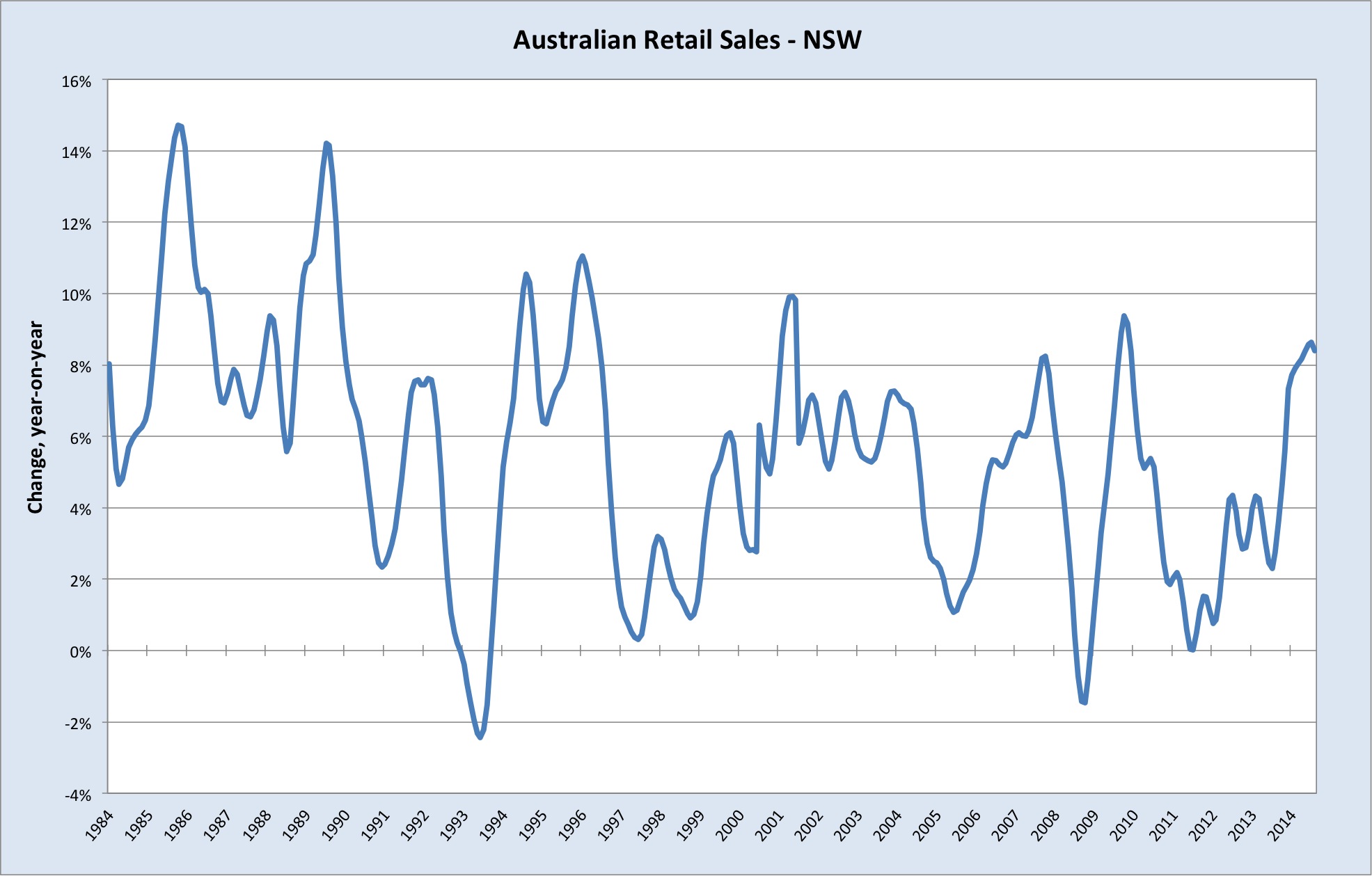

Those industry groupings cover businesses benefiting from the last monetary easing cycle and the consequent boom in house prices. Unsurprisingly, seeing as it’s the nucleus of the boom, NSW has accounted for over half the increase in capital spending by ‘other selected industries’ over the past year.

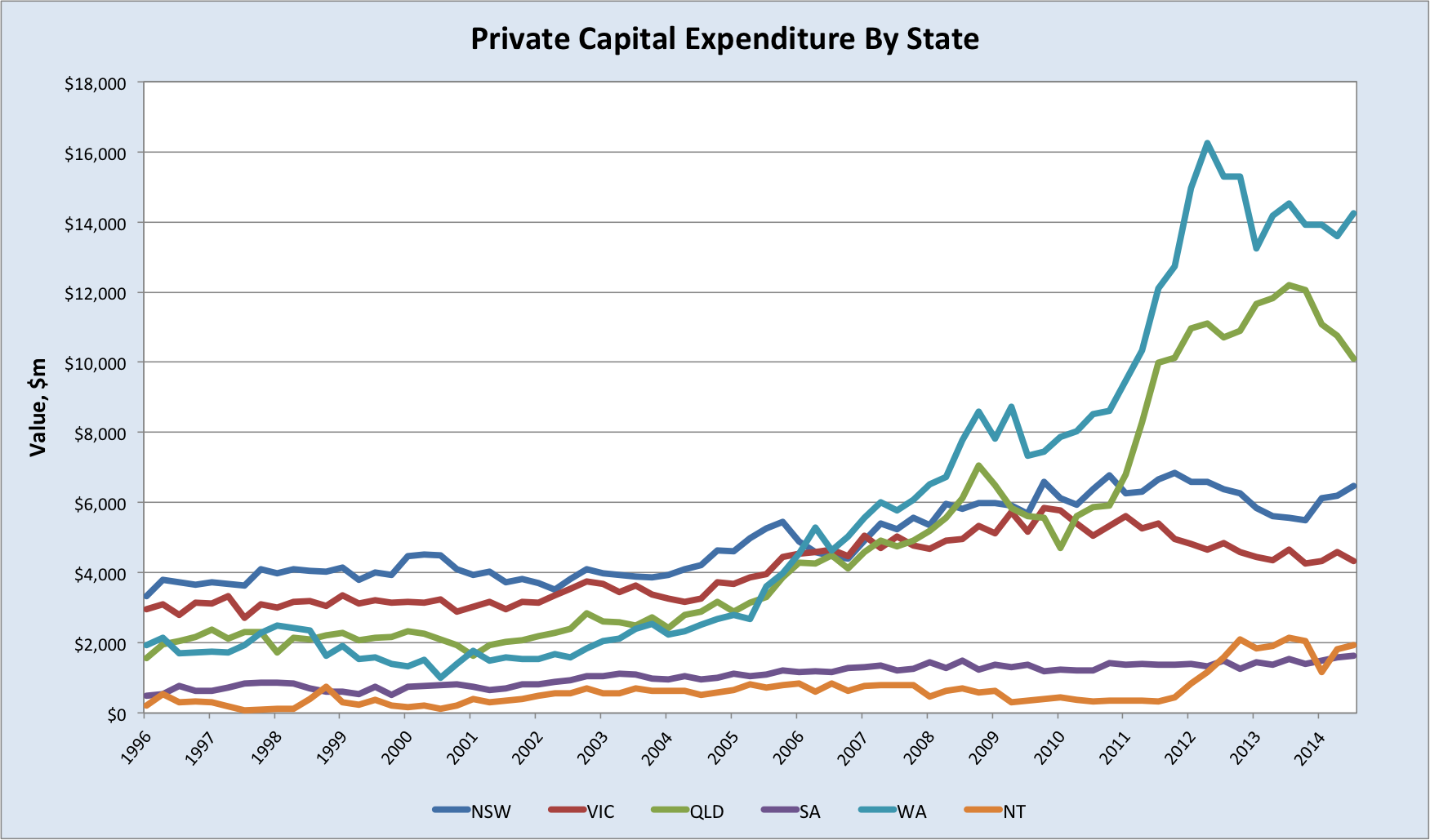

Here’s the division of total capital spending by state.

Evidently, the cyclical boost emanating from the Sydney property sector and the resilience of mining investment in WA have cushioned the overall blow to capital spending in the past year. The latter of those points is important. If capex holds up in WA, it’ll come at the expense of the iron ore price, since capital spending in WA is almost entirely constituted by iron ore capacity expansions.

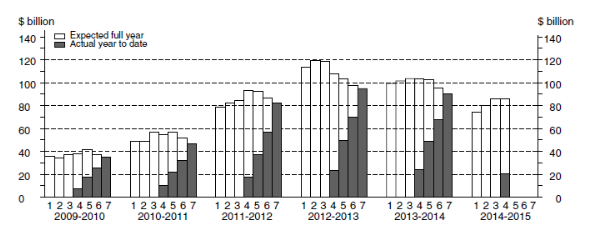

Here are the expectations for capital spending this financial year:

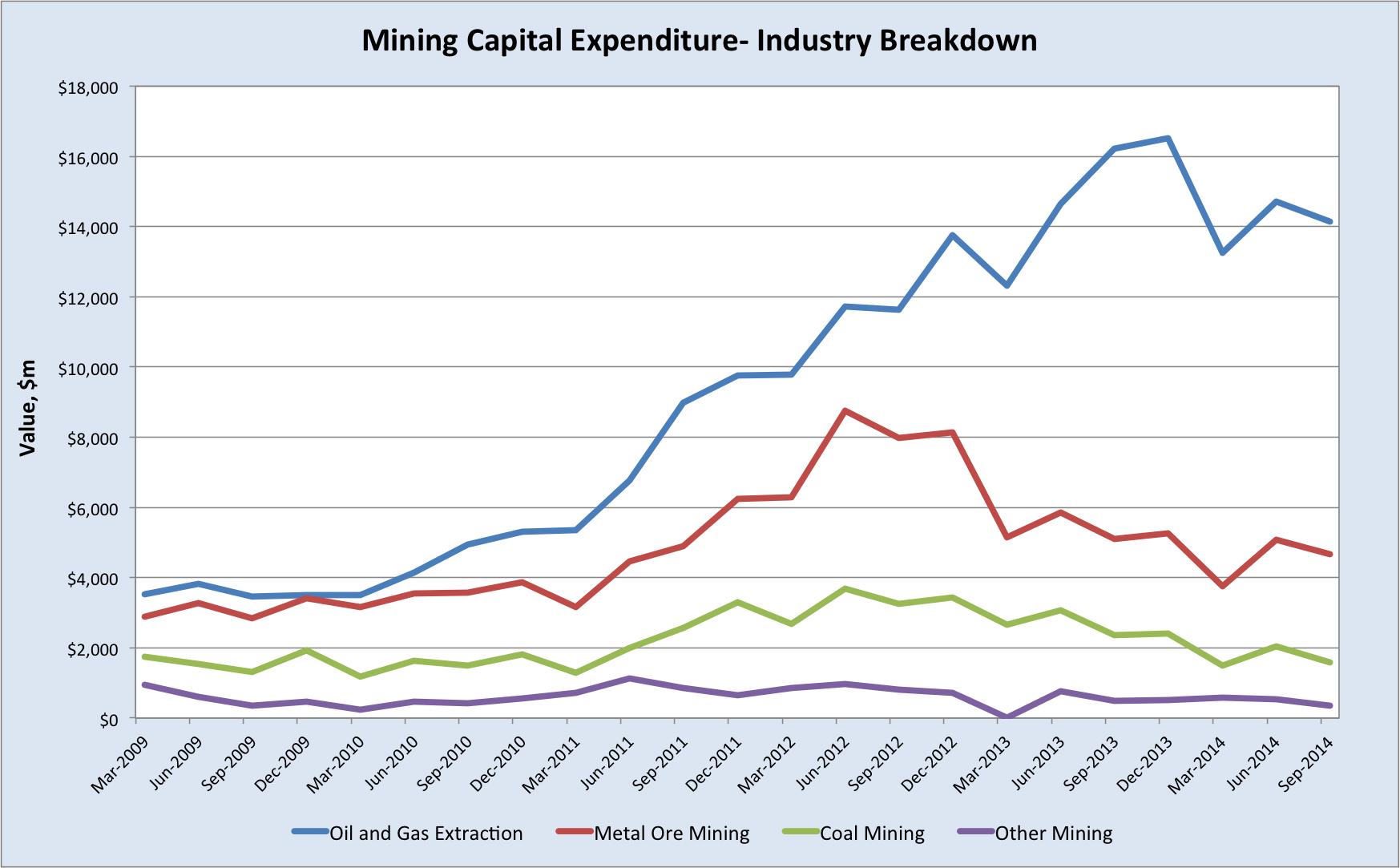

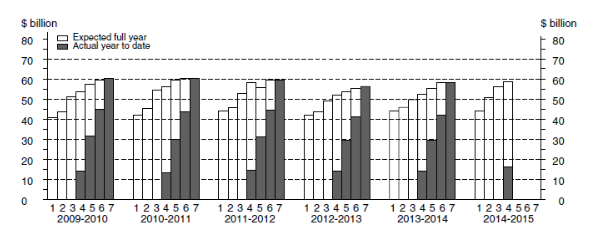

Mining

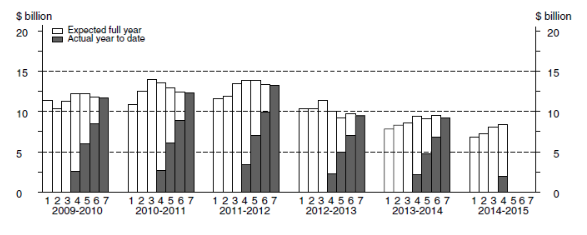

Other Selected Industries

Manufacturing

Manufacturing is all but dead so we can ignore that until we see the dollar fall 20-30% in real terms.

Without further cuts to interest rates, the cyclical upswing in NSW is likely to run out of puff over the next 6 months or so, in which case I wouldn’t be surprised to see expected spending by ‘other selected industries’ moderate somewhat by the time the full year’s spending has been recorded. Activity in this interest rate-sensitive space reflects the RBA’s strategy for ‘rebalancing’ the Australian economy as the resource sector slows. This is bubbly economics: papering over a structural downturn with a cyclical upturn in borrowing, asset speculation and consumption. The US famously tried this strategy after the tech wreck early last decade, and it ended up with a catastrophic housing bust.

Thankfully, Australians have mostly kept their heads so far, and the bubbliest segments of the economy are confined to Sydney property speculation and manic Melbourne apartment building. Credit is not growing too rapidly and household savings rates remain reasonably healthy (bearing in mind, of course, that households are already heavily indebted). Nevertheless, the bubbly segments have lately caused enough consternation within the RBA and APRA for these institutions to move forward with ‘macroprudential regulations’, specifically aimed at reducing macroeconomic risks in the property sector and banking system. Despite having cheered it on, the RBA finally grew wary of the housing beast.

It remains to be seen how stringent macpru ends up being in Australia, but it is a welcome move. Some commentators will be inclined to regard this upturn in housing-related activity as healthy rebalancing, but in my view a structural downturn needs a structural remedy, not a temporary sugar hit. We need a lower real exchange rate and productivity-enhancing reforms and infrastructure spending to boost investment in non-mining tradable goods industries. Until we get that, it’s hard for me to get excited about any purported ‘rebalancing’.

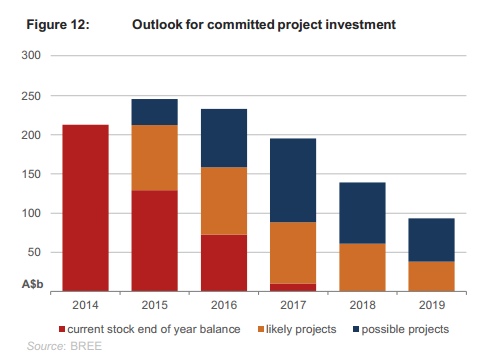

As to mining investment, there’s little doubt that we’re going to see it deteriorate sharply over the next two years, particularly given the recent carnage in iron ore and crude oil prices (which LNG prices are linked to). The BREE recently published its forecasts for mining projects.

It’s safe to say that ‘possible projects’ are extremely unlikely, and also that many ‘likely projects’ will fail to break ground as well, without big rebounds in oil and iron ore prices, or a sharp fall in the Australian dollar.

Bonus Chart